Lastly, you leave the doctor’s office feeling relieved. You show them your insurance card. They inform you that everything is okay. But then, a few weeks later, you receive an envelope in the mail. And it is a bill. A real bill. You have no idea what it is for.

This is what is going on in the lives of all the people in Texas and all over the United States every single day. If you ever found yourself wondering why you still receive an unexpected bill even after your insurance company paid your bills, you are not alone in this case. You are not doing anything wrong. The healthcare billing process is really complex even to those who do it. Let’s now discuss what is really going on in simple terms as you would explain it to your friends.

Key takeaway:

- Insurance is cost-sharing, you always pay deductibles, copays, and coinsurance

- Out-of-network providers at in-network hospitals can surprise bill you

- Billing errors are common and must be verified against your EOB

- You can dispute bills, negotiate balances, and appeal denied claims

- Charity care and financial assistance programs can reduce your bill

Insurance Was Never Meant to Pay 100% of Everything

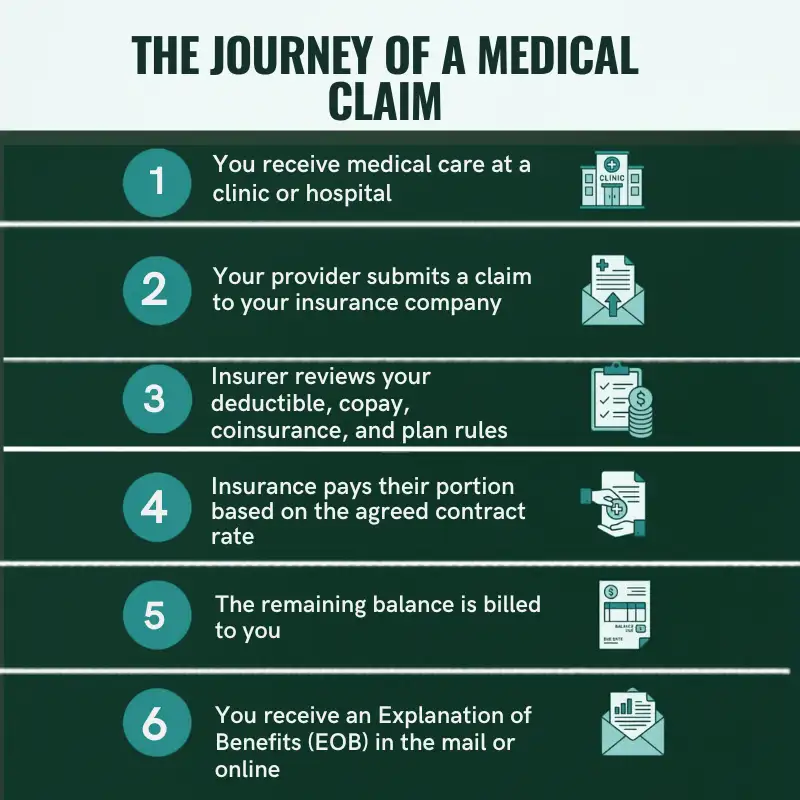

This is the part that most people do not realize until they see the bill. Your insurance plan is designed around a cost-sharing model. That is to say, you andyour insurance company shares the cost of your care based on a series of rules that you agreed to when you signed up for your insurance plan.

When you go to see a provider, your provider is going to submit a claim to your insurance company. They are going to look at your insurance plan and see how much you have paid this year and so on.

Whatever is left over comes to you.

That leftover amount usually falls into a few categories. You might owe the rest of your deductible if you have not hit it yet. You may have a copay, which is a fixed fee for a visit. Once you pay your deductible, coinsurance kicks in. That’s your percentage of the bill. So if the bill is $100 and your coinsurance is 20 percent, you pay $20 and insurance covers the rest.

None of this means something went wrong. It is just how most health plans work in the US.

The Charges That Catch People Off Guard

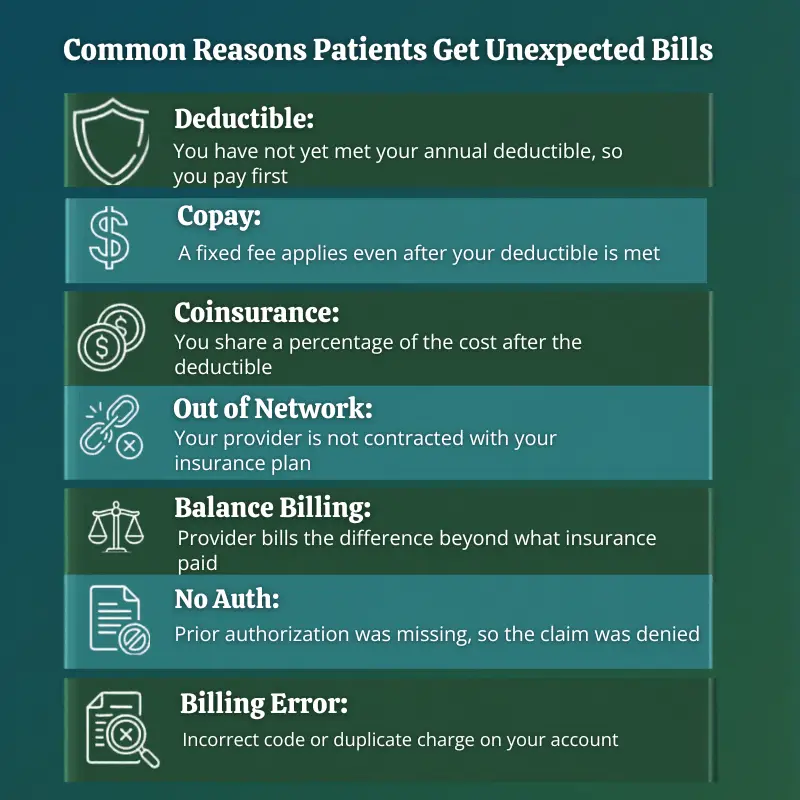

There are certain circumstances that are likely to cause the greatest level of confusion. Knowing these circumstances can prevent you from a great deal of stress and sometimes money.Out of Network Provider at In Network Hospital

This one surprises people constantly. You go to a hospital that is in your network. You think an in-network hospital means all your doctors are in-network too. Wrong. The anesthesiologist or specialist they bring in might be completely out of network. The anesthesiologist or specialist they call in could be out of network.

He can bill you for this treatment himself, and he can do so at a higher rate, even though he is in an in-network facility. This is often referred to as a surprise medical bill, and it has caused financial hardship for many patients.

Some federal regulations have been passed to help protect you from this situation, at least in some emergency situations, through the “No Surprises Act.” However, this is not all-encompassing, and it is worth looking at your EOB carefully.

Balance Billing

If the out of network provider charges you more than what the insurance is willing to pay, the provider might send the bill to you. This is referred to as . This phenomenon is far more common than one would think, and the bill could be far higher than what the patient anticipated.

If you receive a bill that is far higher than what you anticipated, this could be the reason. You have the option of disputing the bill and using independent dispute resolution to resolve the matter.

Prior Authorization Denial

Your insurance company requires advance authorization for certain treatments and procedures before you get them. If your provider doesn’t get this approval, your insurance denies the claim. You’ll hear this called a prior authorization denial or medical necessity denial. When it happens, you end up paying the entire bill yourself.

Before any scheduled treatment, call your provider and ask two things. Does your insurance require authorization? Have they already gotten it?

Billing Errors in Healthcare Are More Common Than You Think

Not every unexpected bill is your actual responsibility. Sometimes the bill itself is wrong.

Billing errors in healthcare happen regularly. A provider might use an incorrect CPT code, which changes the entire meaning of the claim. Sometimes the same service shows up twice on your bill. Your provider might enter your insurance information wrong when they submit it. Or a charge sneaks through for something that should have been bundled into a bigger procedure.

One particularly serious type of error is called . This is when a provider bills for a more expensive service than the one you actually received. It inflates the cost and can lead to denied claims or higher out of pocket charges.

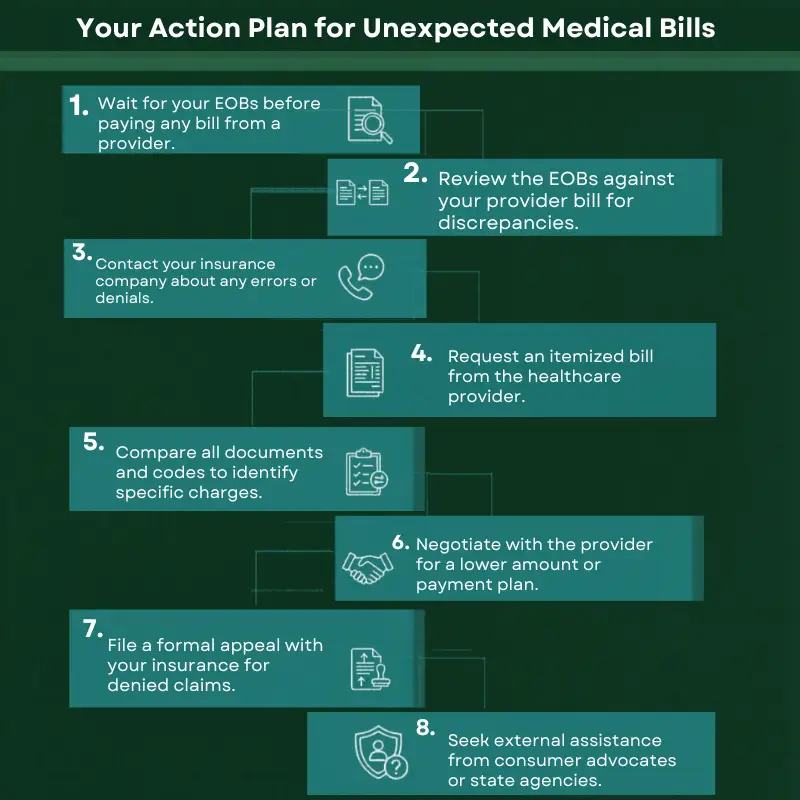

This is exactly why you should always request an itemized medical bill. Request an itemized bill and you’ll get every charge listed separately. This lets you see exactly what the hospital charged you for. If something looks strange, you have every right to ask about it.

If you notice a problem, you should not pay the bill and go about your day. Ask your provider’s billing office to correct it. If the insurer denied a claim based on a billing mistake, you can file an appeal. The more you understand about , the better protected you are.

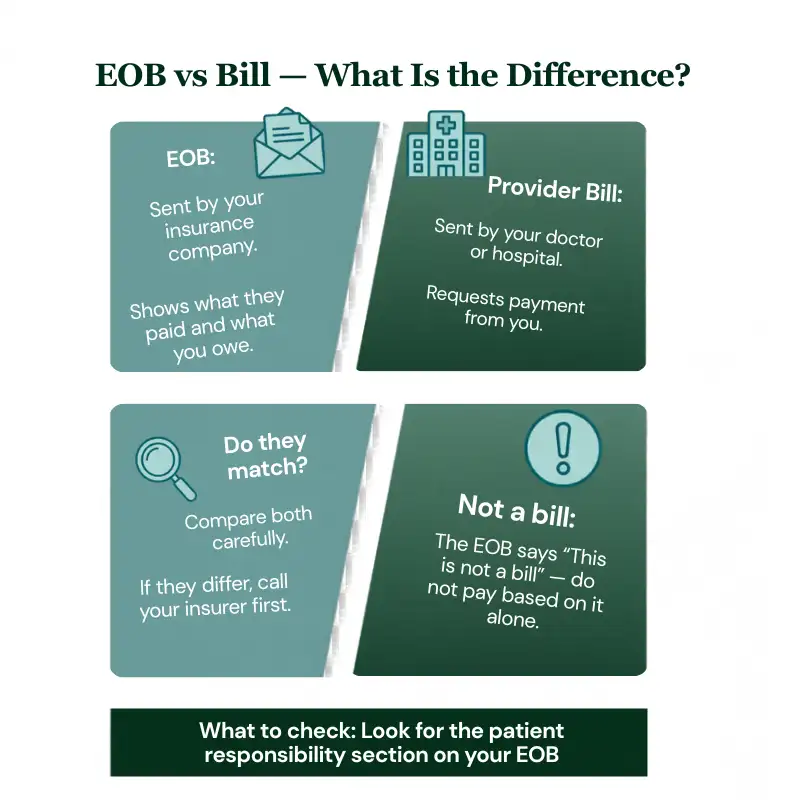

What Is an EOB and Why Does It Matter So Much?

Once your insurance processes a claim, you will receive a document called the Explanation of Benefits, or EOB. The most helpful thing you can do for yourself is to understand the difference.The EOB is not a bill. Your EOB shows you four key things: what your provider charged, what your insurance actually paid, what adjustments they made, and what you owe. The bill from your provider should match up with what the EOB says you owe.

However, if these two documents are not matching, then this is also a cause for concern. This tells you one of three things actually happened. Someone made a billing error somewhere in the process. The claim got processed incorrectly by your insurance company. Or your provider is charging you more than what your insurance contract allows.

Wondering to process? In most cases you will receive your EOB within a few weeks of the service. If you get a bill from your provider before you get an EOB, wait for the EOB before paying anything.

How to Negotiate Medical Bills After Insurance, And Actually Win

Most people assume medical bills are fixed. They are not. You can question them, negotiate them, and in many cases reduce them significantly.

Here are some real that work.

First, always ask for an itemized bill. You have a legal right to one. Once you have it, look for duplicate charges, charges for services you did not receive, or anything that does not match what is on your EOB.

Second, ask about . Most hospitals, especially nonprofit ones, have charity care programs. These programs can reduce or eliminate your bill if your income falls within certain guidelines. Ask your hospital specifically about charity care programs. Don’t feel embarrassed asking. Hospitals created these programs specifically to help people in your situation.

Third, ask what the is for your service. This is the maximum your insurer will pay for that service. If the provider billed more than this, the adjustment on your bill should reflect that.

Understanding can also help you determine if the math works.

Fourth, if you think that the claim has been denied incorrectly, then you should appeal the decision with your insurance company.

If you can’t resolve the dispute on your own, you can use independent dispute resolution. A neutral third party listens to both sides and makes a final decision about who’s right. This is especially useful in cases involving out of network charges.

If You Are Drowning in Medical Debt, You Have Options

Sometimes the bills pile up and it starts to feel like there is no way out. is a real option that many people do not know about. You can often negotiate directly with a hospital or provider to settle the balance for less than the full amount, especially if the debt has been sitting unpaid for a while.

Looking into is another step worth taking. State programs in Texas, federal programs, and nonprofit organizations can all provide support depending on your situation.

If you are feeling overwhelmed and unsure of your rights, then you should consider seeking the help of a . These are experts who can assist you in reviewing your bills, identifying any errors, and negotiating on your behalf in order to determine what you are actually paying for. This can result in huge savings.

Transparency in hospital pricing is also something you can use to your advantage. Hospitals are now required to post their prices publicly. Checking a hospital’s price list before a planned procedure, something called , can help you compare costs and plan ahead.

Quick Patient Checklist

- Did you receive your EOB from your insurance provider?

- Does the EOB match the bill received from the provider?

- Did you request a full itemized medical bill?

- Did you check for any duplicate charges or errors on the bill?

- Did you check to see if you qualify for any kind of financial assistance or charity care?

- Did you check to see if prior authorization was obtained, if required?

- Did you appeal the claim unfairly denied by the insurance provider?

A surprise medical bill happens when you get care at an in network facility but one of your providers, like a specialist or anesthesiologist, is out of network. You end up billed for the difference. Federal law now offers some protection against this in emergency situations.

Start by requesting an itemized bill and comparing it to your EOB. If you find an error, call the provider’s billing office and ask for a correction. If the insurer denied a claim incorrectly, file a formal appeal. You can also contact your state insurance commissioner for help.

Ask about charity care eligibility, financial assistance programs, and payment plans. You can also negotiate the bill directly. Many hospitals will accept a lower lump sum if you ask. A medical bill advocate can help you navigate this process and spot savings.

An adjustment is a reduction in what you owe. It often reflects the difference between what the provider billed and what your insurance agreed to pay under their contract. If your bill shows an adjustment, it is usually a good thing. It means the provider cannot charge you the full original amount.

In Texas, most insurance claims are processed within 15 to 45 days. If a claim is taking longer, call your insurer to ask for a status update. Delays can sometimes be caused by missing documentation or coding issues that your provider may need to correct.

The Team at Integrate Point Is Here for You

Integrate Point Can Help, Receiving a bill after insurance pays is normal. It doesn’t mean you should accept it blindly. Read your EOB. Compare it to your bill. Request an itemized statement. Check for errors. Look for assistance programs. If the bill still doesn’t add up, push back.

You have more options than you think.

Integrate Point helps clinics and patients in Texas and across the US decode medical billing, spot errors fast, and challenge unfair charges. You shouldn’t navigate this alone. Let us help you make sense of your bills and recover money you shouldn’t owe.

This Post Has One Comment

Never knew this, regards for letting me know.