You pay a copay at the doctor’s office. Then a bill arrives for something else entirely. Most people don’t understand the difference between copay and coinsurance, which is why surprise medical bills catch them unaware. The truth is, it’s not complicated. Let’s simplify it for you.

Key Takeaway :

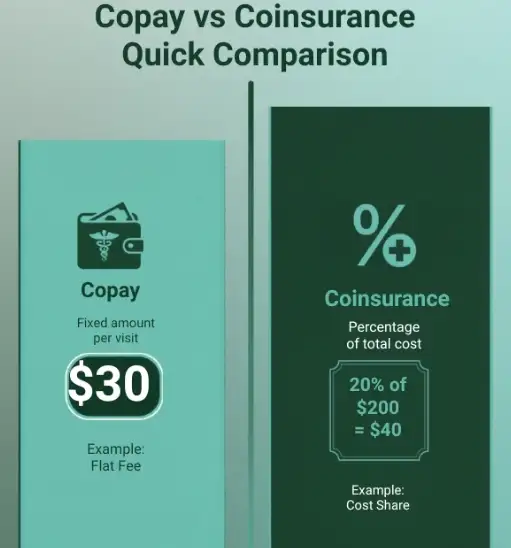

- Copay is a fixed amount you pay at each visit ($25, $50, etc.)

- Coinsurance is a percentage of the bill that comes later (usually 20%)

- Both affect your healthcare costs but work differently

- Understanding the difference prevents surprise bills

- It’s simpler than insurance companies make it seem

What Is a Health Insurance Marketplace?

What is a health insurance marketplace? A health insurance marketplace is like a shopping mall, Instead of looking for clothes to buy, you will look for insurance to buy. You go to a website and look at all the health insurance plans all the insurance companies have to offer. Then you can pick the health insurance you think is best for you. The health insurance marketplace is just there to make sure all the health insurance plans are qualified.

If you are from Texas or any state in the US, there is something called Healthcare.gov. It is a marketplace that you can shop from to buy insurance. States also have individual marketplaces. What is important to know is that there is money that is charged to your account. This is where copay and coinsurance are used.

What Is a Copay in Health Insurance?

A copay is really simple. You’re going to be paying a certain amount of money every time you visit a doctor or fill a prescription. This is it. You always know exactly how much money you’re paying before going to the doctor or filling a prescription.

For example, let’s say that the copay for a doctor visit is twenty-five dollars. This means that every time you visit your primary care doctor, you’re paying that twenty-five dollars.

Your insurance company is paying the rest.

Copays are predictable. That’s their biggest advantage. You budget knowing you’ll pay that same amount every visit. Whether the doctor spends five minutes or thirty minutes with you doesn’t matter. You still pay twenty five dollars.

What Is Coinsurance in Health Insurance?

Coinsurance works differently. Instead of a fixed amount, coinsurance is a percentage. You pay a percentage of the actual bill. Your insurance company pays the rest.

Here’s a real example. Say you go to the hospital and the bill is one thousand dollars. Your plan has twenty percent coinsurance. You pay two hundred dollars. Your insurance company pays eight hundred dollars. Simple math, but the amount changes depending on how expensive the service is.

Coinsurance usually applies to bigger expenses. Hospital stays. Surgeries. Special tests. These are the expensive services that can really hurt your wallet. That’s why understanding coinsurance matters. It affects the bigger medical bills.

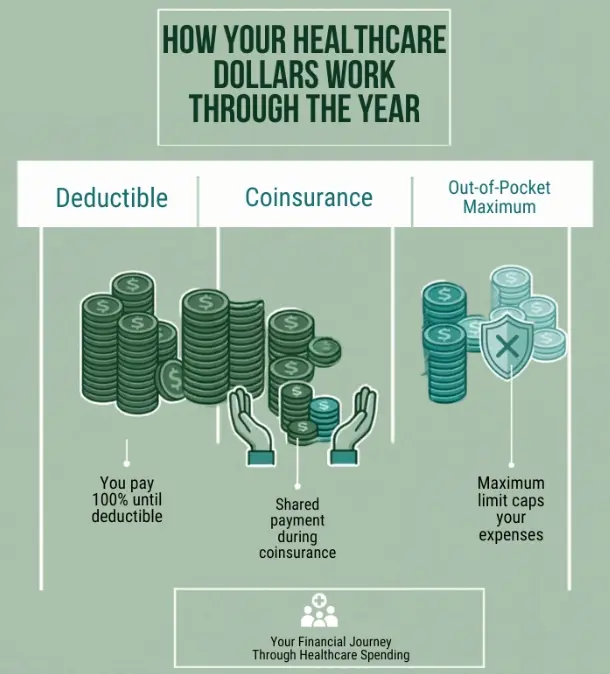

Understanding a Deductible Plan

A deductible is the money you have to pay yourself before your insurance starts helping. Think of it like a door you have to walk through before insurance kicks in.

Let’s say your plan has a two thousand dollar deductible. Your doctor visits, hospital stays, and prescriptions all come straight out of your own pocket. You’re paying for everything yourself until you hit that two thousand dollar limit. Once you’ve paid two thousand dollars out of your own pocket, then your insurance finally starts helping pay your bills.

Your copays might apply before hitting your deductible, depending on your plan. Some count toward it. Coinsurance works differently. It’s confusing because different plans do it different ways. This is where reading your actual plan document matters.

How Copay and Coinsurance Work Together

Here’s how it typically goes in real life. First, you have a deductible. You pay the full cost of everything until you hit that deductible amount. Once you’ve paid your deductible, one of two things happens.

If your plan uses copays, you then pay your fixed amount per visit or prescription. Your insurance starts paying their share.

If your plan uses coinsurance, you then pay a percentage of bills. Your insurance pays the rest until you hit your out of pocket maximum for the year.

Some plans use both. You pay a copay for the office visit. Then you pay coinsurance for any tests the doctor orders during that visit. Confusing? Yes. But that’s how some plans work in Texas and across the country.

Which Is Better for Your Situation?

There’s no perfect answer that works for everyone. It really depends on how much you use healthcare.

If you go to doctors a lot because you have a chronic condition, lower copays save you money. You visit frequently, so the fixed amounts add up nicely. You can budget knowing exactly what each visit costs.

If you’re generally healthy and barely see a doctor, you might prefer a plan with a higher deductible and coinsurance. The monthly premium might be cheaper. You gamble that you won’t get seriously sick. If you do, coinsurance means you’re splitting the expensive bills with your insurance company rather than paying the full amount yourself.

The key is thinking about your own situation. How many times do you typically see a doctor each year? Do you take medications regularly? Do you have any chronic health conditions? Answer these questions honestly, and you’ll get a better sense of which payment structure helps your wallet.

Medical Billing Errors and What to Watch For

Here’s something most people don’t know. Medical billing errors happen all the time. Sometimes you get charged for something you shouldn’t, or the bill gets sent to your insurance wrong. Sometimes copays and coinsurance get calculated incorrectly.

You get a bill and you should check it. Look at the services listed. Make sure they’re things you actually had done. Check that copays match what your plan says. Look at those coinsurance calculations. If something looks wrong, call the office. Ask questions. Don’t just pay it because the bill says so.

You also might get what’s called balance billing. This happens when a doctor charges you more than your insurance allows. They bill you the difference. In Texas and many other states, laws limit balance billing. But it still happens. Understanding your copay and coinsurance helps you spot when balance billing is happening to you.

Insurance Eligibility Verification

Before you get care, your doctor’s office often checks your insurance. Your doctor’s office checks that your coverage is active, confirms your deductible status, and determines which copay or coinsurance applies to your specific service.

This process saves you problems. It stops surprise bills. It speeds up insurance claims processing. Before you book an appointment, don’t be shy about calling your insurance company or asking your doctor’s office to verify your coverage. It takes five minutes and saves major headaches.

Preventive Care Services at No Cost

Here’s something great about marketplace plans. Preventive care services are free. Vaccinations. Cancer screenings. Annual checkups. Blood pressure checks. These all happen at no cost even before you meet your deductible.

But remember, each plan has an out of pocket maximum. That’s the total amount you’ll pay in a year for all your medical care combined. Once you hit that number, your insurance pays one hundred percent for the rest of the year. This limit protects you from medical bankruptcy if you get seriously ill or injured.

Key Differences You Should Know

Understanding health insurance terms helps you navigate bills, choose plans, and avoid surprises. Here’s what separates copay from coinsurance from deductible.

A copay is a fixed fee. Coinsurance is a percentage. A deductible is the first money you pay before insurance helps. Each one affects your healthcare expenses differently. Knowing the differences means smarter choices about your coverage and your wallet.

Tips for Patients in Texas

In the Texas area, many insurance plans work slightly differently depending on whether you use an in network provider or go out of network. Your copay might be ten dollars in network but fifty dollars out of network. Your coinsurance might be twenty percent in network but forty percent out of network.

Before you go into a doctor’s appointment, you should always check your insurance plan. Before you go in, check that your doctor is part of the plan, find out if you need a referral, and ask what the procedure might cost you. This way, you can avoid any unexpected medical expenses.

There are many healthcare systems that offer financial counseling. If you are struggling with your medical bills, you can always get financial counselling. There are also departments in hospitals that can assist you if you cannot afford your medical bills.

You still pay your copays. But you also pay full price for services until your deductible is met. After the year ends, your deductible resets. Next year, you start over. You won’t meet your deductible.

It depends on your plan. Most plans have networks of doctors. Using in network doctors means lower copays and coinsurance. Out of network doctors might cost significantly more. Always check before scheduling.

No. Preventive care services are always free under marketplace plans. They don’t count toward your deductible. This is one of the best parts of these plans.

Copay is fixed. You pay the same amount every time. Coinsurance varies with the bill. A larger bill means a larger coinsurance payment.

Doctors have two different prices. They charge different amounts depending on your insurance company. Your copay or coinsurance might be based on an allowed amount that’s less than what the doctor actually bills.

Managing Your Healthcare Expenses

The difference between copay and coinsurance helps you manage your medical bills. Understanding the difference really helps you make smarter choices about which doctors you visit, know what your bills should cost when they arrive, and spot any errors before paying them.

Start by reading your plan documents. Yes, they’re boring and confusing. But they explain exactly what you’ll pay and when. Call your insurance company with questions. Visit their website. Use their cost estimator tools. These resources exist to help you understand your coverage.

Keep records of your medical expenses. Write down when you see doctors. Note how much you pay in copays and coinsurance. This helps you track whether you’re hitting your deductible or approaching your out of pocket maximum. It also helps you catch medical billing errors because you know what you should have paid.

Ask for an “Explanation of Benefits” from your insurance company for each claim made. This shows you exactly how much you paid, how much your insurance company paid, and what it means in total. Read it, check for errors, and call your insurance company or doctor if you have a concern about what you see.

Final Thoughts

Copay versus coinsurance. Deductible versus out of pocket maximum. These terms don’t have to confuse you. Understanding them actually takes just a few minutes. And that understanding can save you hundreds or thousands of dollars in unexpected medical costs throughout the year.

Whether you live in Texas or anywhere else in the United States, your healthcare marketplace plan works the same way. You have copays, coinsurance, a deductible and an out of pocket maximum. Knowing how each one works means you’re in control of your healthcare costs rather than being surprised by them.

Take time to understand your specific plan. Write down your copay costs, coinsurance percentage, deductible, and out of pocket maximum so you know them when bills arrive. Write these numbers down. Keep them where you can find them. If you are sitting in a doctor’s waiting room or trying to read a bill, knowing these numbers can help you quickly understand what you need to pay.