You’re shopping for health insurance and suddenly you’re drowning in acronyms. HMO. PPO. EPO. POS. What do these even mean? Why do they matter? Understanding the difference between HMO, PPO, EPO, and POS plans means you stop guessing and start choosing wisely.

Key Takeaway:

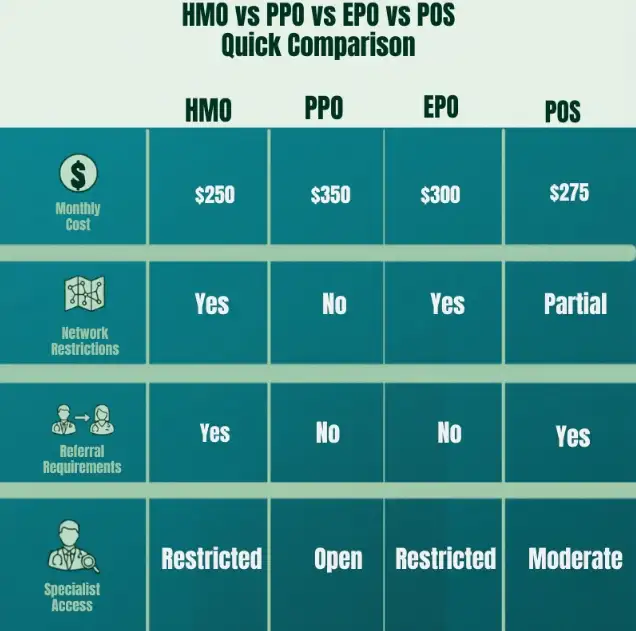

- HMO is cheapest but most restrictive with network limitations and referral requirements

- PPO offers maximum flexibility to see any doctor but costs significantly more

- EPO provides specialist access without referrals while keeping costs lower than PPO

- POS combines HMO cost savings with PPO flexibility through out-of-network coverage

- Choose based on your actual healthcare needs, preferred doctors, and budget—not what you think you should pick

What Is an HMO Plan Really?

An HMO is a Health Maintenance Organization. Think of it as the budget option for health insurance. You pay lower monthly premiums. You pay lower copays. But you make tradeoffs.

Here’s how an HMO plan works. First, you pick a primary care doctor. This is your gatekeeper. Every time you need specialist care, you go to your primary doctor first. They write you a referral. Then you can see the specialist. If you try to see a specialist without a referral, the insurance won’t pay.

Second, your doctor has to be in network. The HMO plan only covers doctors who work with that insurance company. If you go to an out of network doctor, you pay the full bill yourself. The only exception is emergencies. If you’re having a heart attack, you go to whatever hospital is closest. The HMO will pay for that emergency care.

HMO plans work great if you like your primary doctor and that doctor is in network. You know exactly what your costs will be. Everything is coordinated through one doctor who knows your complete medical history.

What Is a PPO Plan and Why Do People Love It?

PPO stands for Preferred Provider Organization. This is a flexibility plan. You pay higher monthly premiums and higher deductibles. But you get much more freedom.

With a PPO, you don’t need a primary care doctor. You don’t need referrals to see specialists. You can see any doctor you want whenever you want. Your insurance will pay more if you use network doctors, but they’ll still pay for something even if you go out of network.

This matters. Say you need to see a cardiologist. With an HMO, you call your primary doctor, get a referral, and wait for an appointment. With a PPO, you can call the cardiologist directly tomorrow and schedule an appointment. No waiting. No referral is needed.

PPO plans cost more. Your premiums might be two hundred dollars higher each month. Your deductible might be higher. But if you like having choices, if you travel frequently, if you have doctors, you really trust, a PPO might be worth the extra cost.

What Is an EPO Plan?

An EPO is an Exclusive Provider Organization. This is the middle-ground option. It’s less well known than HMO or PPO, but it’s worth understanding.

An EPO plan doesn’t require a primary care doctor. You can see any specialist directly without a referral. That’s the freedom part. But you have to use network of doctors. If you go out of the network, the insurance won’t pay except for emergencies. That’s where it’s like an HMO.

An EPO plan costs less than a PPO but more than an HMO. You get some freedom without paying the full PPO price. It’s a reasonable compromise for people who want direct access to specialists but don’t need unlimited out of network coverage.

EPO plans to work well if you’re generally healthy. You probably won’t need specialists very often. But when you do need one, you want to be able to call and schedule without jumping through referral hoops.

What Is a POS Plan?

A POS is a Point of Service plan. This combines features from HMO and PPO plans. It’s like a hybrid option.

A POS plan requires a primary care doctor and referrals for specialists, just like an HMO. But unlike an HMO, a POS plan provides some coverage for out of network care. You’ll pay more to go out of network, but you’re not completely uncovered.

A POS plan costs more than an HMO but less than a PPO. It gives you most of the cost savings of an HMO with more flexibility when you really need it.

A POS plan makes sense if you want to save money, but you’re worried that being locked into a network might be a problem. You get the coordinator of care of an HMO with a safety net for emergencies or special situations.

Comparing the Four Plans Side by Side

All four plans work differently, have different costs. All four fit different people’s situations.

An HMO plan has the lowest cost but the least flexibility. A PPO plan has the highest cost but the most flexibility. An EPO plan offers flexibility without the PPO price. A POS plan offers flexibility plus an out-of-the-network safety net.

Which plan is best for you? That depends on your situation. Are you healthy? Do you have any preferred doctors? How much does money matter to you? The answer to these questions determines which plan makes sense.

HMO Plan Pros and Cons

HMO plans have real advantages. Your monthly premium is the lowest of all four option, copays are predictable and low. Your care is coordinated through one doctor who knows your complete medical history. This coordination can actually improve your health outcomes.

But HMO plans have real disadvantages too. You’re locked into a network. If your favorite doctor isn’t in network, you can’t see them. You need referrals for specialists. That takes time. If you travel frequently, you might not be able to see your doctors when you’re away from home.

PPO Plan Pros and Cons

PPO plans give you freedom. You can see any doctor. You can see specialists without referrals. Your insurance covers out of network care. This matters if you travel, if you have specific doctors you trust, or if you want maximum flexibility.

But freedom costs money. Your premium, deductibles are high. Your out-of-pocket maximum is usually higher. If you go out of network, your out-of-pocket costs jump significantly. PPO plans are great if money isn’t your main concern, but they’re expensive if you’re trying to save.

EPO Plan Pros and Cons

EPO plans to balance cost and flexibility. Your premiums are lower than PPO. You get direct access to specialists without referrals. You don’t have a primary care gatekeeper controlling your care.

But EPO plans have limitations. You’re locked into the network. Going out of the network means paying full prices. The network might be smaller than PPO networks. You might have trouble finding the specific doctors you want.

POS Plan Pros and Cons

POS plans give you balance between cost and flexibility. They’re cheaper than PPO, so your wallet definitely feels the difference. Going out of network still gives you some protection instead of leaving you stranded. Plus, your primary doctor coordinates all your care, which means someone actually knows your full medical story.

But POS plans aren’t perfect. You need referrals for specialists. You’re mostly locked into network. If you value maximum flexibility, a POS plan still has more restrictions than a PPO.

Choosing the Right Plan for Your Situation

Think about your actual life, not what you think you should choose. How many times per year do you see a doctor? Think about whether you have a doctor you actually like seeing. Consider how often you’re on the road traveling. Factor in whether you deal with chronic conditions that require specialist care.

If you barely see a doctor and you don’t have favorite doctors, an HMO or EPO makes sense. Save money on premiums and copays. If you see doctors frequently or have specific doctors you want to keep seeing, a PPO or POS makes more sense. Pay more for flexibility.

Be honest about out of network needs. Will you go out of network, or are you just worried about it? If you’re just worried, an HMO or EPO is fine. If you know you need out of network coverage, PPO or POS is better.

Special Considerations for Texas Patients

In Texas, both urban and rural areas matter. In Dallas, Fort Worth, Austin, San Antonio, and Houston, all four plan types are available. Urban areas have plenty of doctors in network.

But in rural Texas, networks might be smaller. Your local hospital might not be in network. Before choosing an HMO or EPO, check whether your local doctors and hospitals are on network. That research matters more than the plan type.

Many Texas employers offer PPO plans as a benefit. If your employer offers a PPO, take advantage of it. You’re paying partially through employer contributions. The additional cost might be worth flexibility.

How to Actually Compare Plans

Get the official documents for each plan. Look for three things. First, check the monthly premium. Second, check the copays and deductibles. Third, check whether your preferred doctors are in network.

Use your state’s health insurance marketplace or your employer’s plan comparison tool. Enter your preferred doctors and see what plans cover them. That single step eliminates plans that don’t work for you.

Call the insurance company directly with questions. Ask about specific doctors. Ask about whether you need referrals and ask about out of network coverage. Don’t rely on summaries. Get specific answers.

| Plan Type | Referral Needed | Out-of-Network Coverage | Cost | Flexibility |

|---|---|---|---|---|

| HMO | Yes | Emergency only | Low | Low |

| PPO | No | Yes | High | High |

| EPO | No | Emergency only | Medium | Moderate |

| POS | Yes | Yes | Medium | Moderate |

Why This Decision Matters

Your choice of plan affects your healthcare access and your wallet. The wrong plan can cost you thousands of dollars per year in premiums and out of pocket costs. The right plan saves you money and reduces stress about getting care.

Take time with this decision. Read the plan documents. Ask questions. Compare options. Your health and your finances depend on getting this right.

All plans cover emergency care regardless of network status. Emergency room visits are covered. If you’re admitted to the hospital through an emergency, they must stabilize and treat you. You might face higher costs, but you’re covered.

Yes, during open enrollment periods. Most people can change plans once a year. If you have a qualifying life event like marriage, birth, or job loss, you can switch outside open enrollment. Texas follows federal rules for this.

No. PPO plans don’t require a primary care doctor. You can see any doctor directly. You don’t need a gatekeeper. This is one of the main advantages of PPO plans.

Referrals themselves are free. You don’t pay for the paperwork. But when you see the specialist, you pay your copay or coinsurance like any other visit. The referral just lets the insurance know you need specialist care.

HMO requires a primary care doctor and referrals. EPO doesn’t. You get more direct access with EPO but limit you to network providers except for emergencies.

Key Takeaways About Choosing Your Plan

Understanding the difference between HMO, PPO, EPO, and POS plans gives you power. You stop feeling confused, start making informed decisions. You save money by choosing the right plan instead of just picking the cheapest option.

Remember these basics. HMO is the cheapest but most restrictive. PPO is most expensive but most flexible. EPO offers flexibility without PPO pricing. POS offers balance between HMO and PPO.

Your choice depends on your actual life. Not what you think you should choose. Not what others recommend. Your life, your doctors, your budget, your needs.

Take time to compare options. Check your preferred doctor. Ask questions. Make an informed decision. The time you spend now on this choice pays off in savings and peace of mind throughout the year.

This Post Has 9 Comments

Hello, I enjoy reading through your article. I wanted to write a little comment to support you.

My partner and I stumbled over here coming from a different page and thought I might check things out. I like what I see so i am just following you. Look forward to finding out about your web page yet again.

I think the admin of this website is in fact working hard in support of his website, as here every stuff is quality based stuff.

When someone writes an piece of writing he/she keeps the thought of a user in his/her brain that how a user can know it. So that’s why this paragraph is outstdanding.

I’m not that much of a internet reader to be honest but your blogs really nice, keep it up! I’ll go ahead and bookmark your site to come back down the road. Many thanks

Good write-up, I’m regular visitor of one’s blog, maintain up the nice operate, and It is going to be a regular visitor for a long time.

Outstanding writing, as always.

I’m genuinely inspired — thank you so much!

This post was a joy to read — thank you!