You open your mailbox, and there’s the insurance bill. You think, “Wait, I’m paying for all of this?” Your insurance is meant to cover your medical bills, right? But then you see things like “deductible,” “copay,” and “coinsurance.” Your head spins. Here’s the truth: most folks don’t really get what a deductible is, and that’s costing them money. Hundreds or thousands of dollars a year in Texas and all over the place. Once you grasp your deductible, you know what you’re paying. Let’s look at this in a way you can relate to.

Key Takeaways:

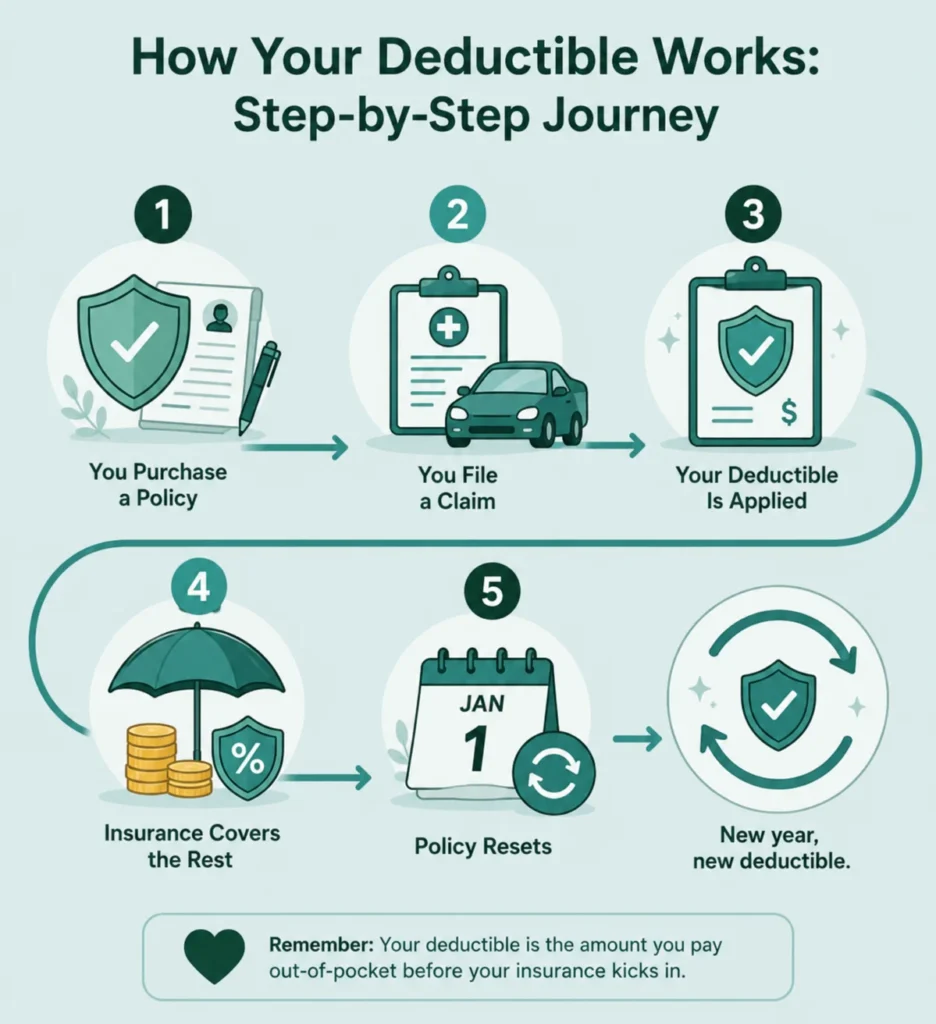

- Your deductible is what you pay first before insurance helps. It resets every January 1st.

- Even after meeting your deductible, coinsurance kicks in usually 80/20 split between you and insurance.

- Preventive care is always free. Use in-network doctors and ask about payment plans before procedures.

- Out-of-pocket maximum is your spending ceiling for the year. Once you hit it, insurance covers 100 percent.

What Does It Mean to Meet Your Deductible?

Your insurance company is essentially saying: “You’re gonna pay a little bit of that medical bill. After you hit that number, we’ll jump in and help.” That first chunk? That’s your deductible.

Let’s say your deductible is $1,500. Each time you visit the doctor or have tests run this year, you’re spending your own money. You get a doctor’s visit for $150. Blood work for $300. An X-ray for $400. You add this all up until you get to $1,500. That’s when you meet your deductible. That’s when your insurance finally says, “Alright, we’re in now.”

But here’s what nobody tells you: even after you meet your deductible, you’re still paying something. You’ve got copays and coinsurance on top of it. The insurance company doesn’t take over completely after that magic number. They just start helping.

How Your Deductible Actually Works: Real Example

You’re at home and your knee hurts. You go to your doctor. The bill is $150. You pay it. Your deductible countdown: $1,350 left. A couple weeks later, your doctor says, “Let’s run blood tests to check your thyroid.” Bill is $300. You pay it. Deductible countdown: $1,050 left. Then you twist your ankle at urgent care. Bill is $800. You pay it. Deductible: down to $250 now. Then you get dental work. You pay $250 toward your deductible, and boom. You’re done. From this point on, your insurance helps pay for stuff. But remember, you’re still not getting everything free. You’re just splitting costs now.

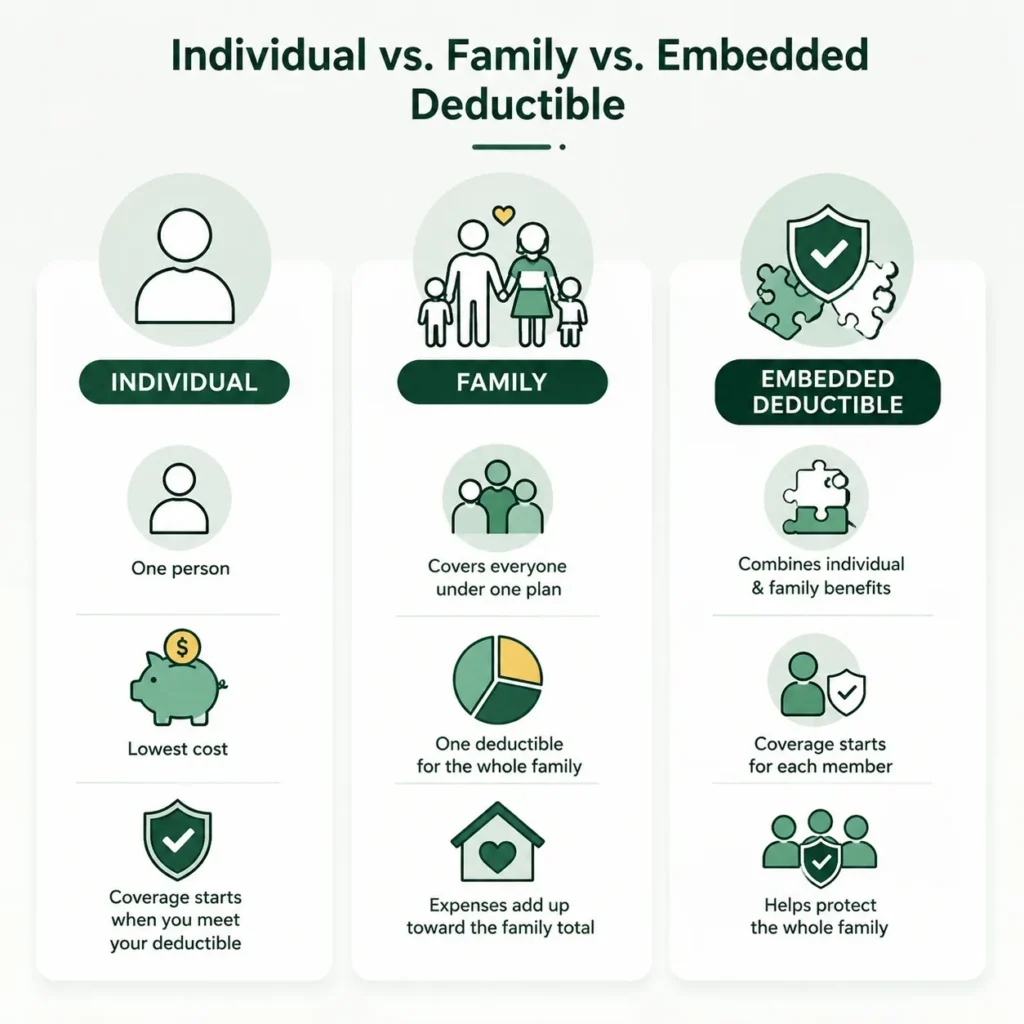

Individual Deductible vs. Family Deductible: Which One Do You Have?

If you’re on your own plan, this is simple. Your deductible is just yours. If you’re covering your family, there are two different ways family deductibles work.

Individual Deductible: Each person has their own separate number. You have $1,200. Your husband has $1,200. Your daughter has $1,200. They don’t share. Everyone’s on their own until they hit their number.

Family Deductible with Built-In Individual Coverage: Your plan says “Individual deductible is $1,200. Family deductible is $3,000.” Each person still has their own $1,200. But here’s the good part: once your kid hits their $1,200, insurance starts covering their stuff. They don’t wait until the whole family reaches $3,000.

Family Deductible with No Individual Safety Net: The whole family has one number. Let’s say it’s $4,000. Everyone’s bills add together. Once the family hits $4,000 total, everyone gets coverage. This is tough on families where only one or two people need healthcare.

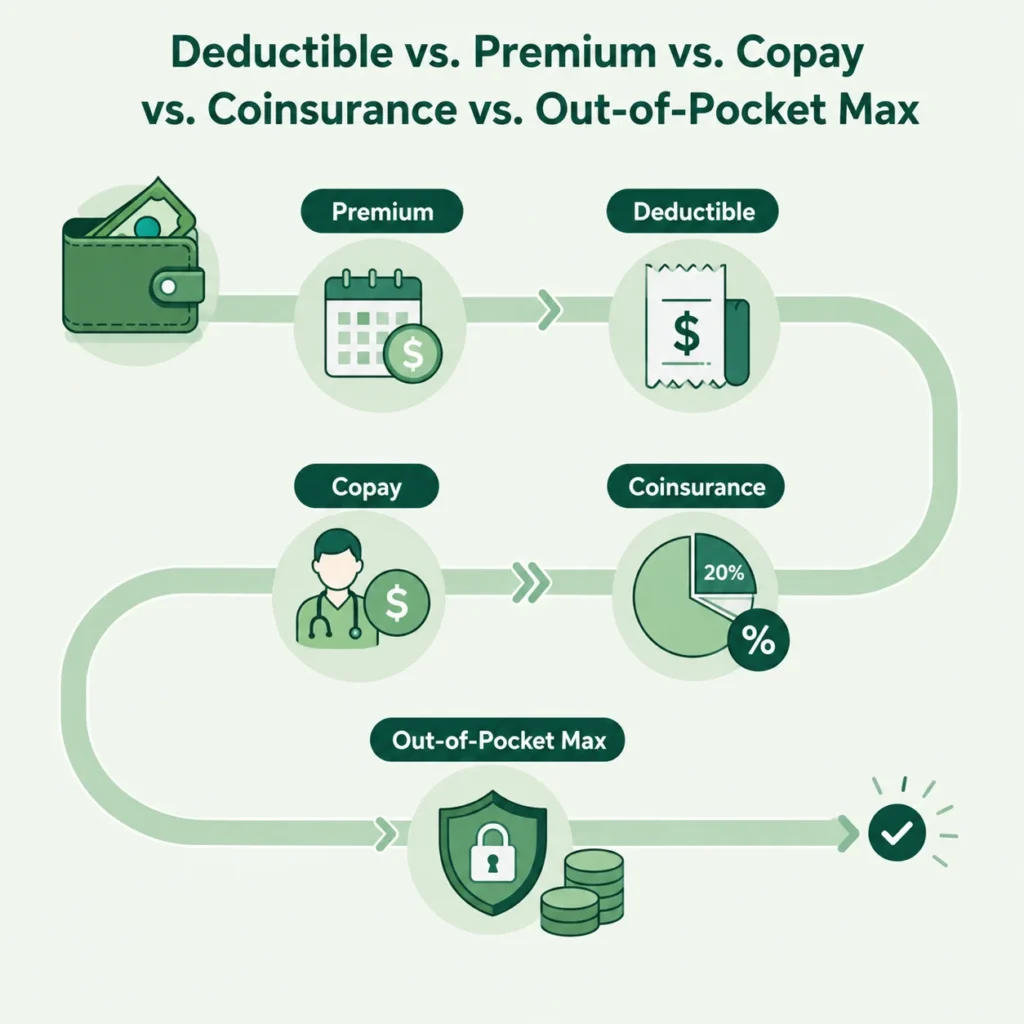

Deductible vs. Premium: Stop Mixing These Up

People think deductible and premium are the same thing. They’re not. Your premium is money you pay every single month to keep your insurance active. You could go the entire year without seeing a doctor and you’re still paying your premium. You don’t get that money back.

Your deductible is different. It’s money you pay when you actually use your insurance. When you go to the doctor, you get tests. When you need a procedure. You only pay it if you use your insurance. Here’s the trade-off: plans with cheaper monthly premiums usually have really high deductibles. You pay less every month but way more when you actually need the doctor. Plans with higher premiums usually have lower deductibles. You pay more upfront but less when you get sick.

Coinsurance After Deductible: The Surprise Nobody Sees Coming

You finally hit your deductible. You’re thinking: “Great, now insurance takes care of stuff.” Wrong. Even after your deductible is done, you’re still not paying zero. Something called coinsurance shows up. The insurance company pays a percentage, and you pay a percentage. Most commonly, it’s 80/20.

Let’s say you need emergency surgery and you’ve already met your $1,500 deductible. The surgery costs $10,000. With 80/20 coinsurance, insurance pays $8,000. You pay $2,000. That’s why some plans have an out-of-pocket maximum. Once you hit that number like $5,000 for the year, insurance finally takes over 100 percent.

Out-of-Pocket Maximum vs. Deductible: Know Your Ceiling

Think of your deductible as the gate. Your out-of-pocket maximum is the roof. The absolute highest you’ll pay in a year.

Say you have a $1,500 deductible and a $5,000 out-of-pocket maximum. Your deductible is the first $1,500 you pay. After that, coinsurance kicks in. You’re paying 20 percent, insurance pays 80 percent. Everything you pay now counts toward that $5,000 max. Your deductible, copays count, & Your coinsurance counts. All of it. Once you hit $5,000 total for the year, you’re done paying. Insurance covers everything at 100 percent after that.

Paying Your Deductible Before Surgery: What You Should Know

You need surgery. You haven’t met your deductible yet. The hospital calls and says, “We’re going to need around $3,000 from you before we do this.” You panic. Do you really have to pay that much upfront?

Yeah, most hospitals will ask you to pay your deductible and estimated coinsurance before surgery. But don’t freak out. First, hospitals usually have payment plans. Call them and ask. Second, some hospitals have financial hardship programs. If you’re struggling, they can help. Third, get a clear estimate before surgery so you know exactly what you’re looking at.

Free Stuff: Healthcare Services You Don’t Have to Pay For

Here’s good news. Not everything requires you to meet your deductible first. Under the Affordable Care Act (ACA), preventive services are provided at no cost when received from an in-network provider. Learn more on Healthcare.gov.

What’s included? Annual wellness checkups. Free. Flu shots. Free. Cancer screenings like mammograms and colonoscopies. Free. Blood pressure checks. Free. Cholesterol checks. Free. Diabetes screening. Free. Counseling for smoking or weight loss. Free. Well-baby and well-child checkups. Free. The big catch: this only works with in-network doctors. Go out of network and they can charge you. Also, this is preventive stuff. If the doctor finds something wrong, like a lump needing a biopsy, that biopsy isn’t free anymore.

The Annual Reset: Your Deductible Starts Over Every January

On January 1st, your deductible resets to zero. It doesn’t matter if you paid $10,000 toward your deductible in December. Come January 1st, you’re starting fresh. You’re back to zero.

Some people time their medical procedures. If you know you need expensive care like elective surgery, some folks try to get it done before the year ends to maximize their out-of-pocket max benefit. Others wait until January to start fresh if the deductible isn’t a barrier.

Copay and Deductible: How They Fit Together

A copay is that fixed amount you pay when you walk into the doctor’s office. Twenty-five bucks for your regular doctor. Fifty bucks for urgent care. A hundred bucks for a specialist. You pay it when you check in. That’s it.

Here’s the tricky part: copays usually don’t count toward your deductible. You pay the copay separately. So with a high-deductible plan, you might have cheap copays at the doctor’s office but you’re still working on that huge deductible for hospital stuff or surgery. A lot of people don’t realize this until they get a bill and think, “Wait, I already paid my copay, why am I paying more?” Welcome to coinsurance.

How to Actually Save Money on Healthcare

Now you get deductibles. But how do you actually pay less? First, use in-network doctors. Out-of-network is expensive. Double or triple the cost sometimes. Second, try telemedicine. A quick video call costs way less than an office visit. Third, go to those free preventive care visits. Get your annual checkup. Get your screenings. These catch problems early, and early problems are way cheaper to fix. Fourth, ask about cash discounts. Some hospitals will give you a discount if you pay upfront. Fifth, if you get a big hospital bill, ask for an itemized bill and look for errors. Billing mistakes happen constantly. Sixth, negotiate a payment plan if needed. Hospitals will work with you. Seventh, if you have a chronic condition, ask about patient assistance programs.

Using a Calculator to Plan Ahead

Most insurance companies have a calculator or app where you can see what you’ll actually spend in a year. During open enrollment, use this tool. Let’s say plan A has a $200 premium and a $3,000 deductible. Plan B has a $400 premium and a $500 deductible. Which costs you less? Depends on how much you’ll use healthcare. If you see a specialist every month and take three medications, the low-premium, high-deductible plan costs way more. If you’re healthy and barely get sick, the low-deductible plan is a waste of money. Run the numbers. Spend 20 minutes and you could save yourself thousands.

Deductible Aggregate: Your Family’s Total Bill

You’ll see this term on family plans sometimes: deductible aggregate. It’s just a fancy way of saying the total amount your whole family pays together. If your family deductible aggregate is $3,500, that’s the number. Once the family reaches $3,500 total, everyone’s covered. It doesn’t matter if mom paid $3,000 and dad paid $500. The math just matters.

Out-of-Network Doctors: Why They Hurt Your Wallet

An out-of-network provider is a doctor or hospital your insurance doesn’t have a contract with. They cost a ton more. Your insurance might only pay 60 percent instead of 80 or 90 percent. Plus, you might have a separate deductible for out-of-network stuff.

Always check before you book an appointment: is this doctor in my network? Your insurance company’s website has a search tool. Use it. A couple of minutes checking could save you hundreds. If you need a specialist and the good one is out of network, call your insurance. Sometimes they’ll approve it or give you a better rate.

Zero Deductible Plans: Are They Worth It?

Some plans offer zero deductible. Sounds amazing, right? No deductible. You just pay a copay at the doctor’s office. For some people, this is perfect. If you have a chronic condition or go to the doctor a lot, zero deductible is your friend.

But here’s the catch: those plans cost way more in monthly premiums. You’re paying an extra $100, $200, sometimes $300 a month. If you’re paying an extra $200 monthly, that’s $2,400 a year. You’ve got to go to the doctor enough times to save $2,400. For young, healthy people, that doesn’t add up. For someone managing diabetes or regular doctor visits, it might make sense. Run those numbers.

Your deductible doesn’t grow. It stays the same. What changes is how much you’ve paid toward it. Think of it like a countdown timer. You start at $1,500. Every doctor visit or test you subtract from that number. If you spend $300 on bloodwork, your remaining deductible drops to $1,200. You’re chipping away at it. The only time your deductible actually increases is when you renew your plan during open enrollment. Your insurance company might raise it for the new year.

Yes. On January 1st, your deductible resets to zero. Every single year. It doesn’t matter if you paid $5,000 in December. Come January 1st, you start completely fresh. This is why some people time their procedures. Get expensive surgery done before the year ends to maximize your out-of-pocket max benefit. Others wait until January. Either way, the reset is automatic. You don’t have to do anything.

Your deductible is what you pay first. Let’s say it’s $1,500. You visit the doctor, get tests, have procedures. You pay out of pocket until you hit $1,500. That’s when insurance jumps in. Then coinsurance kicks in. You and insurance split costs, usually 80/20. Insurance pays 80 percent. You pay 20 percent. So a $10,000 surgery means insurance pays $8,000 and you pay $2,000. This continues until you hit your out-of-pocket maximum. Then insurance covers 100 percent.

Meeting your deductible means you’ve paid the amount you agreed to pay first before insurance starts helping. Say your deductible is $1,500. Doctor visit $150. Blood work $300. X-rays $400. You add it up. You hit $1,500. That’s the moment you meet it. From then on, insurance starts covering stuff. But you’re not getting everything free. You’re still splitting costs through coinsurance. Meeting your deductible is checkpoint one, not the finish line.

Wrapping It Up: You’ve Got This

You now know what a deductible is, how it works, and the difference between individual versus family deductibles. You understand that preventive care is free, the annual reset happens every January, and out-of-pocket maximums set your spending ceiling. You’ve learned about coinsurance and how costs get split between you and insurance. Honestly, you know more than most people.

Go look at your insurance card and paperwork. Find your deductible number. Write it down. Figure out if it’s individual or family. Understand the number you’re working with. Then when you go to the doctor, you won’t be surprised or stressed. You’ll know exactly what’s happening.

Use the free preventive care. Stay in-network. Ask for cost estimates before big procedures. Make a payment plan if you need to. Just knowing what’s coming makes everything feel less scary. You’ve got this.