Getting the care you need should never feel like a fight. But for thousands of Texas patients and healthcare providers, a denial for a referral or insurance authorization feels exactly like that. One letter and suddenly everything stops. The appointment gets pushed. The procedure gets delayed. The revenue does not come in.

The thing is, that letter is not the end of the road. Most people do not realise they have the right to push back. Knowing how to appeal insurance denial the right way puts you back in control and changes the outcome more often than you would expect.

This guide walks you through every step of that process. Texas rules, real timelines, and resources that actually work.

Referral Denial vs. Insurance Authorization Denial at a Glance

Before you do anything else, you need to know exactly what was denied and why. These two terms get mixed up all the time. People use them like they mean the same thing. They do not. And knowing the difference changes everything about how you respond.

A referral denial usually starts at your primary care provider’s office. Your doctor sends a request for you to see a specialist or get a specific test done. That request does not get approved. It does not happen as often as the other type but it does happen, particularly when your insurance plan requires a formal referral before you can see anyone outside your primary doctor.

An insurance authorization denial is the one most Texas patients and providers deal with on a regular basis. This is when your insurance company decides it will not pay for a service, procedure, medication, or specialist visit before you even receive it. They look at the request and say no before any care is delivered.

The reason they give most often is that the service is not medically necessary by their standards. Sometimes it is not even that. The service might just fall outside what your specific plan covers. Either way the result feels the same. There is something your doctor believes you need and your insurance company is standing in the way of it.

Here is why this distinction actually matters in a practical sense. If you received a referral denial, your first conversation needs to happen with your doctor’s office, not the insurance company. If you received an insurance authorization denial, you go straight to filing a formal appeal with the insurer. Starting in the wrong place wastes time you may not have. Getting this right from the beginning protects both the patient and the practice.

Why Is Your Insurance Claim Being Denied? The Most Common Reasons in Texas

Most denials do not come out of nowhere. There is almost always a specific reason sitting inside that denial letter. The problem is that most people do not know what to look for. Here are the six reasons Texas providers and patients run into more than any others.

1. Not Medically Necessary

The one you will see most often is “not medically necessary.” What that really means is the insurance company looked at your request and decided the service does not meet their definition of essential care.

Here is what stings about that. Their definition and your doctor’s definition are not always the same thing. Your doctor knows your body. The insurer knows their policy.

2. Out of Network Provider

Sometimes the insurance claim being denied has nothing to do with what the service is. It has everything to do with who is providing it.

If the doctor or facility delivering your care is outside your plan’s approved network, the insurer can say no. Even if the care was exactly right for you. Even if there was no other option nearby.

3. Incorrect Coding

Incorrect coding is one of those reasons that feels completely unfair because it is so avoidable. Your provider submits a request and somewhere in that paperwork a code is wrong or a document is missing.

That is all it takes. The insurer has their reason and the denial goes out. One small administrative error can push your care back by weeks.

4. Experimental or Investigational Treatment

Some treatments get flagged as experimental or investigational. Insurance companies keep their own internal lists of what they consider proven and standard.

If your doctor recommends something that sits outside that list, it can get denied regardless of how much clinical evidence supports it. This happens more than most people realize, especially with newer treatment options.

5. Prior Authorization Was Not Obtained

Prior authorization is the step that trips up a lot of providers. Certain services need the insurer’s approval before they are delivered. Not after. Before.

When that approval is not requested, or is requested too late, the claim gets denied the moment it is submitted. The care could have been completely justified, and it still does not matter if the timing was off.

6. Coverage Limitations

Coverage limitations are the quiet ones. Every plan has rules about how often a service can be used, or which diagnoses it applies to.

When a patient’s situation does not fit neatly inside those rules, the insurer denies based on the plan boundaries alone. It is not about the quality of care. It is about what the policy allows.

Your First Step: Read That Denial Letter Carefully!

Your insurance company is required to send you a denial letter—sometimes called an “Explanation of Benefits” (EOB) or “Notice of Adverse Determination.” It will tell you:

- Why was the decision made.

- What specific criteria were used to deny your request.

- How to appeal the decision (step-by-step instructions, deadlines, contact info).

- Your rights to both an internal and, if needed, an external review.

Do NOT delay! Appeal deadlines are strict, so make sure to act quickly.

Step-by-Step: The Insurance Appeal Process in Texas

The appeal process generally involves two main levels: an internal appeal with your insurance company, and if that doesn’t yield a favorable outcome, an external review often managed by the state.

Step 1: Gather Your Information (Your “Appeal Arsenal”)

Before you contact anyone, compile all relevant documents. Having everything ready strengthens your case:

- The Denial Letter: Keep every single page.

- Original referral/authorization request

- Supporting Medical Records: (doctor’s notes, test results, scans, labs)

- Letter of Medical Necessity (LOMN) from Your Doctor: Ask your doctor to write a detailed letter explaining why the service is medically necessary.

- Your Insurance Policy/Summary of Benefits: (check coverage and appeal rules)

- Keep Meticulous Records: Document every interaction: dates, names, reference numbers, copies of letters/emails.

Step 2: Initiate an Internal Appeal

This is your first formal challenge to the insurance company’s decision.

- Contact Your Insurer: Follow the instructions provided in your denial letter (phone, portal, or mail).

- Submit Your Appeal in Writing: state you are formally appealing, list the denied service, patient info, and denial date.

- Attach Everything: Include copies of all supporting documents gathered in Step 1, especially the LOMN from your doctor and your medical records.

- Request an Expedited Review (If Urgent): If your health could be seriously jeopardized by delays (e.g., rapid progression of a condition, immediate need for treatment), you have the right to request an expedited (fast-tracked) appeal.

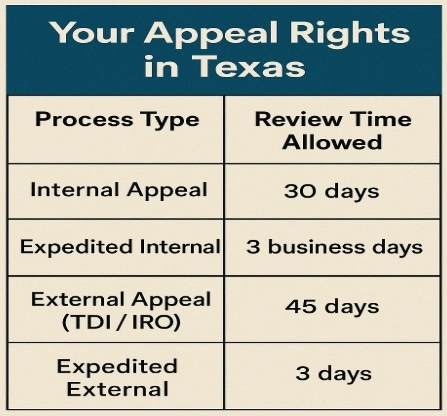

- Texas Timelines for Internal Appeals:

- Standard internal appeals: 30 days

- Urgent cases: 3 business days

Step 3: If the Internal Appeal Fails – Pursue an External Review

If your internal appeal is denied, you are allowed to request an external review.

- Texas Department of Insurance (TDI) oversees external reviews for health insurance plans. The TDI links you with an Independent Review Organization (IRO).

- Independent Review Organization (IRO): This review is carried out by an Independent Review Organization (IRO), a neutral medical panel separate from your insurer, and its decision is usually final and binding on the insurance company.

- How to Initiate: Follow instructions in the internal denial letter or visit www.tdi.texas.gov. You can typically find information and forms under their Consumer Protection section.

- Submit Your Case with the same supporting documentation used for your internal appeal, plus the internal denial letter.

- Texas Timelines for External Reviews:

- Standard external reviews: 45 days

- Expedited (urgent) external reviews: 3 days

Step 4: Additional Resources for Texans

- Texas Department of Insurance (TDI) Consumer Protection: Your primary state resource for help with health insurance issues.

- Texas Health and Human Services (HHS): For Medicaid or CHIP denials

- Patient Advocacy Groups: National or local Texas-based organizations like the Patient Advocate Foundation can offer free guidance and support.

- Legal Counsel: For very complex or high-stakes cases, especially if your health is significantly at risk, consult an attorney specializing in health law (last resort).

Proven Tips to Win Your Insurance Denial Appeal Faster

Most practices that win their appeals are not always the ones with the strongest medical case. They are the ones who moved fast, stayed organized, and never gave up. Here is what thousands of Texas providers have learned the hard way.

1. Act the Same Day

The moment that denial letter lands in your hands, time starts moving against you. Insurance companies set strict deadlines for the insurance denial appeal process. Miss them by even one day and the case is closed.

Do not put the letter in a pile and think you will deal with it tomorrow. Open it today. Read it today. Start your response today.

2. Create One Dedicated Folder

Get a folder. Physical or digital, it does not matter. Put everything in it. Every letter, every email, every fax confirmation.

Texas clinics lose appeals all the time not because their case was weak but because they could not find the right document when they needed it most.

3. Keep Emotion Out of Your Appeal

When you sit down to write your appeal, leave the frustration out of it. The person reviewing your case does not care how unfair this feels. What they care about is evidence.

Show them clearly why this service is medically necessary for this specific patient, this specific diagnosis, this specific situation. Keep it factual. Keep it clinical.

4. Get a Strong Letter of Medical Necessity

Ask your doctor to write a Letter of Medical Necessity. A good one. Not a generic paragraph but a detailed, specific letter that references clinical guidelines and explains exactly why this treatment is the right one.

That letter alone has overturned countless prior authorization denial decisions across Texas. It carries more weight than anything else you can submit.

5. Write Down Every Single Interaction

Every time you call someone about this case, write it down. The date, the name, the reference number, what they said.

That log becomes your most important document if your internal appeal gets denied and you need to take things further with the Texas Department of Insurance. You will be glad you kept it.

6. Read Your Insurance Policy Before You Submit

Before you submit anything, read your insurance policy. Find the exact language about what is covered and what is not.

Many health insurance claim denials in Texas get overturned because the provider simply quoted the policy back to the insurer word for word. Know your plan better than they expect you to.

7. Do Not Stop at One Denial

And when the first appeal comes back denied, do not stop there. A huge number of denied claims get overturned on the second or third attempt.

The system was built to be persistent. So be persistent right back.

FAQ

Most of the time your insurance claim being denied comes down to one of a few reasons. The service was not considered medically necessary by the insurer. Your provider was out of network. Or the paperwork had incorrect coding. Each reason has a fix. Knowing which one applies to you is the first step toward appealing it successfully.

Insurance companies have their own internal criteria for what counts as medically necessary. If your treatment does not match their checklist, they can deny it even if your doctor strongly believes you need it. That is exactly why a Letter of Medical Necessity from your physician carries so much weight in an appeal.

Yes, it happens far more often than it should across Texas providers and patients. A single wrong billing code or a missing document in the request is enough for the insurer to issue a denial.

Coverage limitations are the boundaries your specific insurance plan sets on what it will pay for. Some services are only covered a set number of times per year. Others only apply to certain diagnoses. When your situation falls outside those boundaries, the insurer denies the claim based on plan rules alone.

The first thing Texas providers and patients should do is read the denial letter carefully. It tells you exactly why the claim was denied and what your deadlines are for appealing. Do not wait. The appeal window closes fast and missing it means losing your right to challenge the decision entirely.

Conclusion

Every day a denied claim goes unappealed is a day your Texas clinic loses revenue it rightfully earned. Most denials can be overturned. You just need the right steps and the right support behind you. At Integrate Point, we have helped clinics and independent providers across Texas stop drowning in denied authorizations. We do not just help you appeal. We help you build systems that prevent denials from happening in the first place.From prior authorization management to referral coordination, our Texas based team handles the complexity. Less rework. Fewer denials. Stronger revenue for your practice.

Tired of fighting insurance companies alone? Contact Integrate Point today and let us show you what a cleaner revenue cycle looks like.