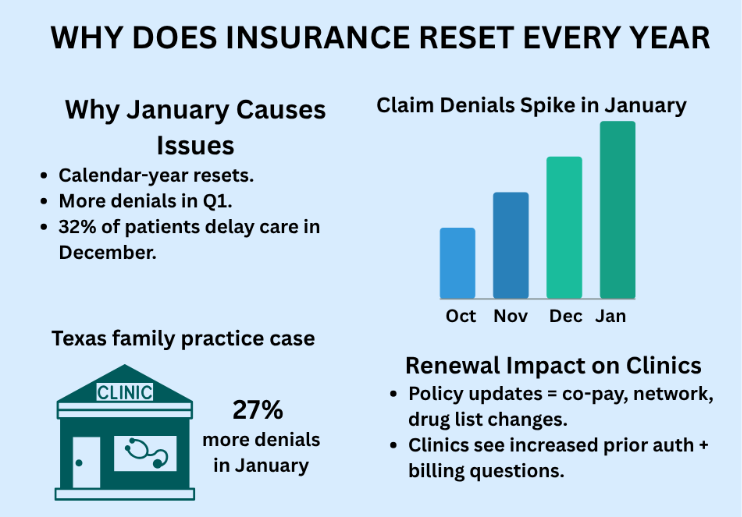

Every January, healthcare providers across Texas face a surge in patient billing questions, claim denials, and coverage verification issues due to insurance resets. While patients think about new year resolutions, clinics, hospitals, and practice managers must navigate deductible resets, insurance renewal dates, and updated coverage rules that directly impact revenue cycles and operational workflows.

- Understanding Deductibles, Out-of-pocket maximum and Renewals, and What It Means for You

- How Insurance Plan Years Work

- Why January Resets Impact Your Deductible, Out-of-Pocket Maximum & Clinic Operations

- Why Do Insurance Companies Reset Plans This Way?

- The Insurance Plan Benefits Might Change

- Required New Prior Authorizations or Referrals

- FSA & HSA Rules May Also Shift

- Planning for the January Reset

- FAQ

- Stay Ahead of January Resets with Integrate Point

Understanding Deductibles, Out-of-pocket maximum and Renewals, and What It Means for You

As the calendar flips to a new year, it’s a natural time for fresh goals and renewed focus—whether that’s improving your health, budgeting smarter, or simply planning ahead. But for those with health insurance, January also signals something else: a reset of your plan’s benefits.

This usually marks the beginning of a new cycle for your annual deductible, out-of-pocket maximum, and other cost-sharing obligations. Understanding this change can help you avoid surprises and make smarter care decisions early in the year.

Let’s break down the “January reset” and what it means for your health coverage.

How Insurance Plan Years Work

The insurance plan year determines when your deductibles, out-of-pocket maximums, and benefit periods reset. For most clinics and patients in the U.S. — including Texas — this aligns with the calendar year, which is why operational disruptions often peak in January.

The core reason for the plan year January reset lies in what’s called your “policy year” or “coverage year”. This is the 12-month period during which your health insurance benefits, deductibles, and out-of-pocket maximums apply.

Calendar Year Plans (Most Common)

For the vast majority of individual and many employer-sponsored health plans, the plan year aligns with the calendar year. This means your benefits period runs from January 1st to December 31st.

Most U.S. and Texas health plans reset every January 1st. This means clinics face increased insurance verification requests, referrals renewal, and billing adjustments at the start of the year.

Non-Calendar Year Plans (Less Common)

Some employer-sponsored plans, particularly for larger companies, might operate on a different schedule, such as a fiscal year (e.g., July 1st to June 30th). In these scenarios, your deductible and benefits are renewed on the first day of your plan’s new coverage period.

Why January Resets Impact Your Deductible, Out-of-Pocket Maximum & Clinic Operations

Most insurance plans include a yearly deductible— a set amount patients must pay out of pocket before coverage starts. This resets to $0 on January 1st, creating a surge in out-of-pocket costs and administrative workload for clinics during the first quarter. When plan year resets, several key components of your health insurance effectively start over:

Deductible

The total amount of money you are required to pay for covered healthcare services before your insurance plan starts to pay its share.

- The Reset: If a patient’s deductible, say, $2,000, and the plan resets on January 1st, any money paid towards that $2,000 in the previous year no longer counts. Patients need to pay the first $2,000 (or the new deductible is) in covered services again in the new year before the insurer starts contributing significantly.

- Impact:

- For Clinics: This can delay collections, increase pre-visit insurance verifications, and cause patient payment confusion.

- For Patients: Higher upfront medical costs early in the year.

- For Managers: Increased call volume and prior authorization renewals.

According to Kaiser Family Foundation, nearly 78% of U.S. patients face higher out-of-pocket costs in Q1 due to deductible resets, and Texas clinics report a 25% rise in insurance verification tasks in January.

Out-of-Pocket Maximum (OOPM)

This is the maximum amount you’re required to pay for covered medical services within a single plan year. Once you pass this point, your insurance policy typically covers medical expenses of the covered services for the rest of the policy year.

- The Reset: Just like your deductible, your out-of-pocket maximum also resets with the new plan year. Any payments that counted towards your OOPM in the previous year no longer apply.

Coinsurance and Copayments

While these typically don’t count towards your deductible (unless specified by your plan), the accumulation towards your out-of-pocket maximum (if applicable) will also reset.

Why Do Insurance Companies Reset Plans This Way?

Annual Risk Assessment

Insurers evaluate the risks and adjust premiums each year based on updated data. Resetting deductibles and maximums annually allows them to manage financial risk and project costs more effectively for each new coverage period.

Standardization

The January 1st reset aligns with the calendar year, making it a straightforward and consistent approach for most individual plans and for open enrollment periods (like those through the ACA Marketplace).

Encourages Preventative Care

Some plans cover certain preventative services (like annual physicals and screenings) before the deductible is met. Knowing your deductible will reset can encourage you to get these services early in the year.

Based on Centers for Medicare & Medicaid Services data, insurers reassess premiums annually, resulting in plan changes for nearly 60% of U.S. policyholders each January.

The Insurance Plan Benefits Might Change

January also marks the start of a new plan year for most insurance policies in Texas. This can come with:

- New copay amounts

- Updated provider networks

- Different covered medications (aka, formulary changes)

- Premium increases

Even if your insurer or plan name hasn’t changed, the coverage might look different than it did last year.

Required New Prior Authorizations or Referrals

Clinics often need to renew prior authorizations and referrals for ongoing care such as physical therapy, specialist visits, or chronic disease management. This is because many approvals expire with the plan year.

Why? Because many approvals are only valid for a specific timeframe or until the end of the plan year. Insurers want a fresh look at the clinical notes and care plan after the year changes. This increases the administrative load for providers in January.

Don’t assume it carries over—check with your provider’s office or insurance carrier

FSA & HSA Rules May Also Shift

Utilize HSAs/FSAs: If patients have a high-deductible health plan, consider contributing to a Health Savings Account (HSA). HSA funds do not expire at the end of the year—they roll over annually and can be used to pay for approved healthcare costs, including the deductible.

Flexible Spending Accounts (FSAs) also offer tax advantages for healthcare expenses, though they typically have “use-it-or-lose-it” rules.

Tip for Clinics: Clinics can proactively educate patients to use HSA/FSA funds to cover deductibles and copays early in the year. Communicating this can improve collections and reduce payment delays.

Planning for the January Reset

Understanding when the insurance plan benefits reset is crucial for clinics, practice managers, and patients. Here’s how clinics, practice managers, and patients can stay ahead of January disruptions:

- Review insurance plan documents early in December. Always check your specific health insurance plan documents or contact your insurer.

- Verify deductible and out-of-pocket balances using payer portals.

- Confirm clinic or provider if prior authorizations or referrals need renewal.

- Review the Summary of Benefits for the new year’s changes

- Budget accordingly for January and February when medical costs may be higher

- Train front-desk staff to handle Q1 insurance reset calls.

- Inform patients about possible changes to copays and coverage.

- Adjust billing cycle forecasts for Q1.

By being informed and proactive, you can better navigate your healthcare costs and make the most of your benefits throughout the entire plan year.

FAQ

1. Why does health insurance reset every January?

Most plans follow a calendar year. Deductibles, copays, and out-of-pocket maximums reset on January 1. Patients may pay earlier in the year, and clinics must update coverage, authorizations, and billing.

2. How can clinics prepare for the reset?

By:

- Verify coverage early

- Renew prior authorizations

- Train front-desk staff

- Inform patients about changes

Integrate Point automates these steps for smoother operations.

3. What does a deductible reset mean for patients?

Patients start paying out of pocket again until the deductible is met. This often means higher costs in January and February. Patients can prepare by understanding their benefits, checking in-network coverage, and using HSA/FSA funds strategically.

4. How does the reset affect prior authorizations and referrals?

Most expire at year-end. Clinics must renew them for continued care.

Integrate Point helps manage prior authorizations and referral renewals and avoid delays.

5. What’s the difference between deductible and out-of-pocket maximum?

Deductible: Amount you pay before insurance kicks in.

Out Of Pocket (OOP) Max: The most you’ll pay in a year before insurance covers 100%.

6. How can clinics and patients avoid surprise medical bills after insurance resets?

- Patients should check plan details and in-network coverage

- Clinics should verify insurance eligibility before visits and communicate estimated costs upfront

- Use Integrate Point services to reduce claim denials and payment surprises.

Stay Ahead of January Resets with Integrate Point

Every January, insurance resets can create confusion for patients and operational challenges for clinics. From rising deductibles to out-of-pocket costs and sudden policy renewals, both patients and providers feel the strain.

We’re Here to Help to Start the Year Strong

At Integrate Point, we work with clinics across Texas to help manage insurance verifications, authorizations, and patient communications. Whether you’re a provider trying to reduce denials, or a clinic improving patient experience—we’ve got the tools and virtual staffing solutions to support your workflow.

January insurance resets don’t have to mean delayed payments and stressed staff.

We help Texas clinics and doctors with:

- Real-time insurance verification

- Prior authorization renewals

- Patient communication and reminders

- End-to-end revenue cycle support

Book a free consultation today and streamline your January workflows with us.