When a baby is born, clinics and hospital teams rush to provide safe discharge, newborn checks, and follow-up visits. But one administrative emergency that often slips through the cracks is insurance enrollment. If a newborn isn’t properly added to a parent’s plan (or to Medicaid/CHIP) in the required window, the family and your clinic can face billing headaches, denied claims, and frustrated parents.

When newborns are not added to Health Insurance plans within the Special Enrollment Period (SEP), hospitals face claim denials, delayed reimbursements, and compliance risks. For parents, it means unexpected hospital bills and coverage gaps. For clinics and revenue cycle teams, it creates avoidable administrative chaos.

Here’s a step-by-step guide for Texas parents on when and how to add your baby to your health plan.

- Why It Matters

- The Cost of Newborn Insurance Enrollment Delays in Texas

- Special Enrollment Period (SEP) for Newborns in Texas: Deadlines by Plan Type

- How to Add Your Newborn

- What Happens If You Miss the Deadline?

- Dual Coverage & the “Birthday Rule”: What Must Be Verify

- Why Hospitals & Clinics Must Be Proactive

- Looking Ahead: Policy Changes to Watch

- Quick Reference Table for Texas

- Final Takeaways

- Conclusion

- FAQs: Newborn Insurance Enrollment in Texas

- 1. How long do parents have to add a newborn to health insurance in Texas?

- 2. Is a newborn automatically covered under the mother’s insurance in Texas?

- 3. Does Medicaid automatically cover newborns in Texas?

- 4. What happens if you forget to add your newborn to your health insurance?

- 5. Can I add my newborn to my Marketplace (ACA) plan after birth?

- 6. Do I need my baby’s Social Security Number to add them to insurance?

- 7. Does adding a newborn increase my health insurance premium?

- 8. How can Texas hospitals reduce newborn insurance claim denials?

- 9. What is the Special Enrollment Period (SEP) for newborns?

- 10. What documents are required to add a newborn to health insurance?

- Stop Losing Revenue on Newborn Claims with Integrate Point

Why It Matters

Medical care for newborns begins immediately—delivery, hospital stay, check-ups, vaccinations, and sometimes specialized care. Without coverage, healthcare costs can add up rapidly. The good news: Texas law and federal rules give you a clear pathway to secure coverage.

The Cost of Newborn Insurance Enrollment Delays in Texas

- Nearly 15–20% of newborn-related claims experience delays due to eligibility errors (AHIP 2024).

- Hospitals lose an average of $250–$500 per newborn case due to retroactive enrollment corrections (HFMA).

- Medicaid covers nearly 53% of births in Texas (KFF, 2024).

- Claims denied due to eligibility issues account for over 25% of initial claim rejections nationwide (MGMA).

Special Enrollment Period (SEP) for Newborns in Texas: Deadlines by Plan Type

The birth of a child qualifies as a “life event,” triggering a Special Enrollment Period (SEP).

- Employer-Sponsored Plans: Typically, you have 30–31 days to notify HR and enroll your baby.

- Marketplace (ACA) Plans: You get a 60-day Special Enrollment Period (SEP) after birth.

- Medicaid/CHIP Perinatal: Many newborns are automatically covered from birth if the mother was eligible.

- Retroactive Coverage: Even if you add your baby later within the window, most plans make coverage retroactive to the date of birth, covering hospital bills and early doctor visits.

Being Proactive Pays Off — Don’t Delay!

- Birth is a Qualifying Life Event (QLE) under federal and state law. It triggers a Special Enrollment Period (SEP), allowing you to enroll your baby in health insurance outside of Open Enrollment. Typically, this window lasts 60 days from the date of birth for Marketplace plans.

- Blue Cross and Blue Shield of Texas specifically allows up to 60 days to enroll a newborn after birth or adoption.

- Employer Sponsored Plans (Including Texas Employees Retirement System):

- 30–31 days enrollment window

- Retroactive to date of birth if completed on time

- Requires documentation (Birth certificate, dependent addition form)

- Missing the deadline = next Open Enrollment

- Texas Senate Bill 896 (Effective September 1, 2025) extends automatic newborn coverage under MEWAs and small Employer plans from 32 days to 61 days — giving families more time but still requiring premium payment within that period for retroactive coverage.

Depending on your insurance type, your window ranges from 30 to 61 days, with 60 days being a common standard.

How to Add Your Newborn

1. Employer-Sponsored Insurance

- Contact your HR or benefits department right away.

- Provide a birth certificate or hospital verification of birth.

- Complete the required forms within 30 days.

2. Marketplace Affordable Care Act (ACA) Plans

- Log into Healthcare.gov or your state’s portal.

- Report birth as a life event.

- Enroll your baby into your current plan or buy a new plan.

- Pay the first premium and upload required documents.

Deadline: 60 days.

3. Medicaid / CHIP (including CHIP Perinatal)

- Babies born to mothers covered under CHIP Perinatal often shift into Medicaid or STAR Health automatically.

- Confirm enrollment with Texas Health & Human Services.

- Call your local Medicaid office if you don’t receive confirmation within 2 weeks of birth.

4. MEWAs & Small Employer Plans

- With SB 896 taking effect on September 1, 2025, parents will now have 61 days to enroll their newborn.

- Premiums must be paid within this period for coverage to apply retroactively.

5. Private / Individual Insurance

- Notify your insurance company directly.

- Submit necessary documentation within the allowed timeframe.

What Documents You’ll Need

- Birth certificate (or hospital record if certificate is pending)

- Social Security Number (can often be submitted later)

- Proof of your current insurance

- Adoption or guardianship paperwork (if applicable)

What Happens If You Miss the Deadline?

- If you miss the 30-day (or 60-day) window, you may have to wait until Open Enrollment (Nov–Jan).

- Your newborn may face a gap in coverage, leaving you responsible for medical bills.

- Employer plans are less flexible, while Marketplace and Medicaid offer more options.

- Always confirm whether your newborn is automatically covered under the mother’s plan for the first 30 days—many plans do, but not all.

- Check if adding a dependent, changes your premium or deductible.

- Retroactive claim corrections increase A/R days

- Deductible and premium adjustments may apply

- Medicaid eligibility may require re-application

Dual Coverage & the “Birthday Rule”: What Must Be Verify

If both parents have insurance, you must decide:

- Which plan to use, or

- Whether to enroll the baby in both.

- Incorrect coordination leads to secondary claim denials

- Always confirm primary payer before first well-baby check ups

If both parents are insured, the primary coverage is generally assigned to the parent whose birthday comes first in the calendar year. This helps coordinate benefits and prevents duplicate billing.

Why Hospitals & Clinics Must Be Proactive

Studies and federal guidance stress that newborn enrollment is time sensitive. Even though parents legally have special enrollment rights after birth, claims can still be denied if the newborn is not added quickly. When hospitals verify insurance and guide enrollment at discharge, there’s fewer denials, faster reimbursement, and fewer retroactive billing issues.

Example: One major hospital that added a mandatory “newborn enrollment checklist” at discharge saw a significant drop in retroactive claim calls within the first year.

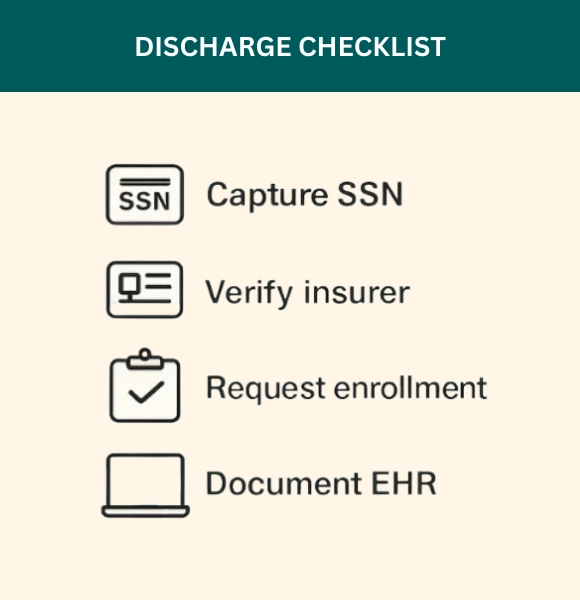

What clinics, discharge teams, and managers should do

Make newborn enrollment part of the discharge and billing workflow:

1. Capture newborn details before discharge

- Ensure the newborn’s Legal name, DOB/time, parents’ names, SSN (if available) are recorded.

- Ask parents which plan they want to use and whether both parents have coverage.

2. Verify insurance + enrollment window

- Check the parent’s insurance. Confirm the insurer’s policy on newborn enrollment windows (30 vs 60 days)

- Confirm Medicaid/CHIP reporting requirements

3. Assist with enrollment

- Provide the family with simple step instructions to add the baby (phone, portal links, insurer instructions)

- If possible, submit a special enrollment request before mother/baby leaves with the parent’s consent.

4. Document everything in the EHR

- Add newborn checklist line: Enrollment requested / pending / confirmed

- Flag account for billing + referral teams to know the newborn’s enrollment status.

5. Follow-up post-discharge

- Send an automated reminder with enrollment deadline + providing insurer links a few days after discharge.

- If enrollment was not completed before discharge, log a follow-up task and re-check coverage before the first well-baby visit

Looking Ahead: Policy Changes to Watch

Beginning in 2026, additional major changes are expected:

- Marketplace premiums are expected to rise sharply—some estimates indicate increases averaging 75%.

- Medicaid and Marketplace eligibility will involve more frequent verification, stricter rules, and potentially less automatic re-enrollment—especially impacting children.

- These changes make timely enrollment and understanding eligibility more important than ever.

Quick Reference Table for Texas

| Plan Type | Enrollment Window | Coverage Effective | Notes |

| Employer-Sponsored Plans | ~30–31 days | Retroactive to birth | Contact HR immediately |

| Marketplace (ACA) Plans | 60 days | Retroactive to birth | Use Healthcare.gov SEP |

| MEWAs / Small Employer Plans | 61 days (from Sept 1, 2025) | Retroactive to birth | SB 896 expands enrollment time |

| Medicaid / CHIP Perinatal | Varies, usually automatic | From birth | Confirm with TX Health & Human Services |

Final Takeaways

For Texas Parents

- Act quickly—your window is short (30–61 days).

- Prepare documents in advance.

- Understand your plan type—rules differ for employer, marketplace, and state programs.

- Don’t risk gaps—coverage protects both your baby and your wallet.

Texas Hospitals & Clinics Must Do to Prevent Newborn Insurance Denials

- Embed newborn enrollment verification into discharge workflow

- Run eligibility verification within 72 hours post-discharge

- Track SEP deadline inside EHR

- Flag newborn accounts pending enrollment

- Automate reminder outreach before deadline

- Audit newborn claims monthly

Conclusion

Newborn enrollment is a small process with big consequences. Make it part of every discharge checklist, automate verification where you can, and assign clear ownership.

At Integrate Point, we help hospitals and clinics automate eligibility checks, manage special enrollments, and reduce billing denials. We can build a newborn enrollment workflow that runs from bedside verification to follow-up reminders, saving staff time and protecting your revenue.

FAQs: Newborn Insurance Enrollment in Texas

1. How long do parents have to add a newborn to health insurance in Texas?

In Texas, the deadline depends on the type of health insurance plan:

- Employer-Sponsored Plans: Typically 30–31 days from the date of birth

- Marketplace (ACA) Plans: 60-day Special Enrollment Period (SEP) through HealthCare.gov

- Medicaid / CHIP: Often automatic at birth if the mother is enrolled, but confirmation is required

- MEWAs & Small Employer Plans (SB 896): 61 days beginning September 1, 2025

Coverage is usually retroactive to the baby’s date of birth if enrollment is completed within the allowed window.

Missing the deadline may require waiting until the next Open Enrollment period.

2. Is a newborn automatically covered under the mother’s insurance in Texas?

In many cases, yes — but only temporarily.

- Most employer and Marketplace plans provide automatic coverage for the first 30 days after birth.

- Medicaid often covers newborns automatically if the mother was eligible at delivery.

- Coverage does not continue beyond the temporary period unless the baby is formally added as a dependent.

Hospitals and billing teams should verify coverage before discharge to prevent eligibility-related claim denials.

3. Does Medicaid automatically cover newborns in Texas?

If the mother was enrolled in Texas Medicaid at the time of delivery, the newborn is generally eligible for coverage from birth.

However:

- Enrollment must still be confirmed with Texas Health and Human Services (HHSC).

- Documentation may be required.

- For mothers covered under CHIP Perinatal, newborns often transition to Medicaid, but follow-up is necessary.

Failure to confirm enrollment can lead to claim delays or billing errors.

4. What happens if you forget to add your newborn to your health insurance?

If you miss the enrollment deadline:

- Employer plans may require waiting until Open Enrollment (Nov–Jan)

- Hospital bills may become the parent’s responsibility

- Claims may be denied due to eligibility issues

- Retroactive coverage may not apply

Marketplace (ACA) plans offer a 60-day Special Enrollment Period, but once that window closes, options become limited.

For hospitals and clinics, missed enrollment increases accounts receivable days and denial rates.

5. Can I add my newborn to my Marketplace (ACA) plan after birth?

Yes. Birth qualifies as a Qualifying Life Event (QLE) under federal law.

Parents have:

- 60 days from birth to enroll the baby through HealthCare.gov

- The option to add the newborn to an existing Marketplace plan

- The ability to select a new Marketplace plan

Coverage is retroactive to the date of birth if enrollment is completed on time.

6. Do I need my baby’s Social Security Number to add them to insurance?

Not immediately in most cases.

Parents can usually:

- Submit enrollment first

- Provide the Social Security Number (SSN) later once issued

However, documentation such as a birth certificate or hospital record is typically required.

Hospitals should advise families to complete enrollment even if the SSN is pending.

7. Does adding a newborn increase my health insurance premium?

Yes, in most cases.

Adding a dependent may:

- Increase monthly premiums

- Change deductible amounts

- Adjust out-of-pocket maximums

Employer Sponsored Plans and Marketplace plans calculate premiums based on family size.

Parents should confirm updated premium amounts before the next billing cycle.

8. How can Texas hospitals reduce newborn insurance claim denials?

Hospitals and clinics can reduce eligibility-related denials by:

- Verifying insurance before discharge

- Confirming the Special Enrollment Period deadline

- Documenting enrollment status in the EHR

- Sending post-discharge enrollment reminders

- Running eligibility checks before the first well-baby visit

Proactive workflow management significantly reduces retroactive billing issues and improves reimbursement timelines.

9. What is the Special Enrollment Period (SEP) for newborns?

A Special Enrollment Period (SEP) allows parents to enroll a newborn in Health Insurance outside of Open Enrollment.

In Texas:

- Employer plans: ~30 days

- Marketplace (ACA) plans: 60 days

- MEWAs (after SB 896): 61 days

The birth of a child is considered a life-changing event, triggering this enrollment opportunity under federal law.

10. What documents are required to add a newborn to health insurance?

Commonly required documents include:

- Birth certificate (or hospital verification of birth)

- Social Security Number (if available)

- Proof of current insurance

- Dependent enrollment form

- Guardianship or adoption paperwork (if applicable)

Submitting documents early helps prevent delays in claim processing.

Stop Losing Revenue on Newborn Claims with Integrate Point

Integrate Point helps Texas hospitals and clinics:

- Automate newborn eligibility verification

- Track Special Enrollment Period deadlines

- Reduce eligibility-based claim denials

- Improve Medicaid & Marketplace enrollment documentation

- Protect revenue during discharge workflows

We’ll identify eligibility gaps, denial risks, and missed enrollment deadlines in your current process.