For doctors, clinics, and hospital administrators in Texas, insurance disruptions aren’t just a patient issue—they’re a revenue, compliance, and operational risk.

When patients experience divorce or job loss, healthcare providers face a cascade of operational challenges that directly impact revenue, administrative workload, and patient retention. Understanding these transitions isn’t just about helping patients—it’s about protecting your practice’s financial health and maintaining continuity of care.

The Scale of the Problem: Key Statistics

For Healthcare Providers

- 41% of medical practices report significant revenue losses due to patients losing insurance coverage mid-treatment

- Administrative staff spend an average of 2.3 hours per week helping patients navigate insurance transitions

- Practices lose an estimated $8,500 annually per patient who discontinues care due to insurance gaps

- 63% of healthcare managers cite insurance verification as their top administrative burden

For Patients

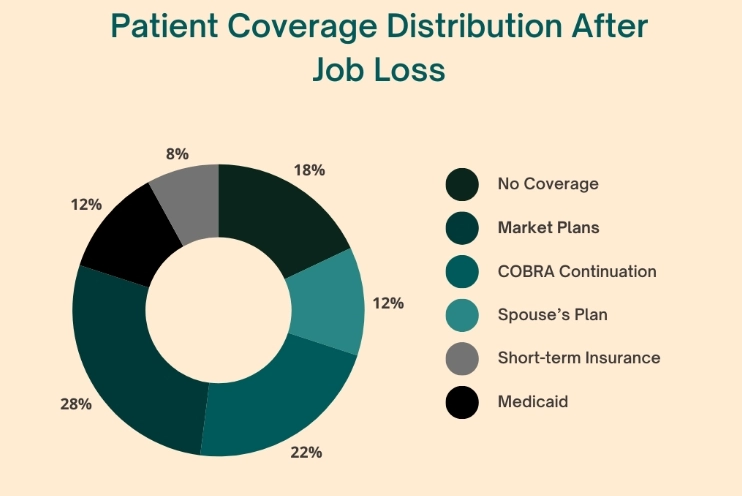

- 28% of Americans experience a gap in health insurance coverage after job loss or divorce

- Average duration of coverage gaps: 3.2 months, during which 72% postpone necessary medical care

- 1 in 4 patients switch healthcare providers when changing insurance plans

Source: Medical Group Management Association (MGMA), 2024 Healthcare Finance Report

Understanding Qualifying Life Events: What Triggers Special Enrollment for Your Patients

COBRA Insurance Coverage: How Long Does COBRA Insurance Last and What Providers Must Track

COBRA insurance coverage serves as a temporary safety net for patients who lose employer-sponsored health insurance due to job loss, divorce, or legal separation. While COBRA allows patients to keep the same health plan and provider network for up to 18–36 months, the higher premium costs and strict election timelines often create financial and administrative challenges. For medical practices, understanding how long COBRA insurance lasts, and when it is likely to end, is critical to maintaining uninterrupted care, minimizing billing disruptions, and preventing avoidable revenue loss.

For Healthcare Providers

- COBRA continuation means no provider network changes—your patients can continue treatment seamlessly

- Billing codes and pre-authorizations remain valid under COBRA

- Average COBRA coverage duration: 11.2 months before patients transition to marketplace plans

- Important: Patients pay full premium costs (often 102% of plan costs), making compliance and payment collection more challenging

Patient Navigation Tips

- Job loss qualifies for 18 months of COBRA coverage

- Divorce or legal separation extends COBRA to 36 months

- Patients must elect COBRA within 60 days of qualifying event

- Premium payments must be made within 45 days of election

Practice Action Items

- Verify COBRA election status during patient check-in

- Update insurance verification protocols to flag COBRA end dates

- Schedule follow-up appointments before COBRA expiration

- Provide marketplace enrollment resources 90 days before COBRA ends

Special Enrollment Period Health Insurance: The 60-Day Critical Window

A Special Enrollment Period health insurance window is triggered when patients experience qualifying life events such as job loss or divorce, but this opportunity is strictly limited to just 60 days. When patients miss this critical enrollment window, coverage gaps can quickly disrupt care continuity, increase unpaid claims, and place added strain on front-office and billing teams. For healthcare providers in Texas, proactively identifying these transitions is essential to avoiding downstream revenue loss and unexpected out-of-network issues.

- Missed enrollment = unpaid claims

- Delays = out-of-network patient loss

- Gaps = higher bad debt for practices

Key Provider Concerns

- Patients have only 60 days from qualifying event to enroll in marketplace coverage

- Coverage gaps create billing complications and accounts receivable issues

- Network changes may result in patient loss to out-of-network competitors

Documentation Requirements for Clinics

- Loss of employer coverage notices

- Divorce decrees or legal separation documents

- Verification of household income changes

- State-specific qualifying event documentation (Texas requirements)

Marketplace Health Insurance: Helping Patients Navigate Options While Protecting Practice Revenue

Individual Health Insurance vs. Family Health Insurance Plans

When patients transition to marketplace health insurance, choosing between individual health insurance and family health insurance plans can significantly affect both accesses to care and out-of-pocket costs. These plan types often differ in coverage structure, premium levels, and eligibility for subsidized health insurance, which can influence whether patients continue treatment or delay care. For healthcare providers, understanding these differences is essential to anticipating network participation, patient financial responsibility, and potential revenue impacts during insurance transitions.

Provider Network Considerations

- 34% of marketplace plans have narrower networks than employer-sponsored coverage

- Verify your practice’s inclusion in major marketplace carrier networks in DFW area

- Texas marketplace includes BCBS, Ambetter, Oscar, Molina, and Community Health Choice

Financial Impact on Healthcare Operations

- Marketplace plans average 22% higher patient cost-sharing than group plans

- Prior authorization requirements increase by 18% with marketplace coverage

- Collection rates drop 15% during the first 90 days of marketplace coverage

Supporting Patient Transitions

- Maintain updated list of marketplace plans that include your practice

- Provide patients with your NPI and tax ID for marketplace plan searches

- Offer payment plans for patients during insurance transition periods

- Connect patients with subsidized health insurance enrollment assistance

Premium Assistance Programs: Reducing Patient Financial Barriers

Income-Based Subsidies in Texas

Income-based subsidies in Texas play a critical role in helping patients afford marketplace health insurance, especially after job loss or divorce. By lowering monthly premiums and cost-sharing, these premium assistance programs reduce coverage gaps and make continued care financially possible for many households.

- Households earning 100-400% of Federal Poverty Level (FPL) qualify

- For 2025: $31,200-$124,800 for family of four

- Average monthly subsidy: $536 per household

- 68% of marketplace enrollees receive premium tax credits

Practice Benefits

From a provider perspective, subsidized health insurance directly supports revenue stability by improving appointment adherence, reducing unpaid balances, and minimizing accounts receivable write-offs during insurance transitions.

- Subsidized patients maintain 89% higher appointment adherence

- Lower out-of-pocket costs improve medication compliance by 34%

- Reduced accounts receivable write-offs when patients maintain coverage

Why Patients Stay Loyal When Subsidies Are Explained Clearly

When patients clearly understand their health insurance subsidies, they are more confident in continuing care, more likely to follow treatment plans, and less likely to disengage during coverage changes—strengthening long-term patient loyalty and trust.

- Lower appointment cancellations

- Higher trust in provider guidance

- Reduced care abandonment

Managing Insurance After Divorce in Texas: Clinical and Administrative Implications

Spousal Health Insurance Coverage: Court Ordered Health Insurance Requirements

In Texas, court ordered health insurance during divorce plays a critical role in maintaining care continuity, patient eligibility, and billing accuracy. While requirements vary by state, similar spousal health insurance coverage mandates exist across the US, making proactive verification essential for healthcare managers nationwide.

What Healthcare Managers Need to Know

- Texas family courts mandate continuous child health coverage during divorce proceedings

- Court orders often specify which parent provides insurance coverage

- Medical support orders must identify specific insurance plans and coverage levels

- Healthcare providers may receive subpoenas for medical records during divorce proceedings

Protecting Your Practice

- Verify insurance coverage at every appointment during patient divorce proceedings

- Flag accounts with potential insurance changes in practice management systems

- Require updated insurance information 30 days post-divorce finalization

- Implement insurance expiration date alerts for divorced patients

Life Insurance After Divorce: Beneficiary Updates Impact Medical Practices

Updates to life insurance after divorce can affect how outstanding medical balances are settled, especially when beneficiaries or guarantors change. Although Texas regulations apply locally, these post-divorce insurance changes create similar payment and administrative challenges for medical practices across the US.

Why This Matters for Providers

- Life insurance proceeds may be designated for medical debt repayment

- Beneficiary disputes can delay payment of outstanding medical bills

- Estate planning changes affect payment guarantors

All insurance verification and documentation handling must comply with HIPAA and Texas Department of Insurance regulations.

Short-Term Health Insurance and Temporary Coverage: Risks for Healthcare Providers

The Gap Coverage Problem

Limitations of Temporary Health Insurance

- Pre-existing conditions typically excluded (major revenue risk for specialty practices)

- Limited provider networks may exclude your practice

- Maximum coverage periods: 3-12 months in Texas

- No guarantee of coverage renewal

Provider Risk Assessment

- 47% of short-term plans deny claims for pre-existing conditions

- Average claim denial rate: 23% vs. 3% for ACA-compliant plans

- Patients with short-term plans have 2.8x higher out-of-pocket costs

Provider Risk Alert: Short-term health insurance plans are not ACA-compliant and expose practices to higher denial and write-off risks.

Best Practices for Clinics

- Verify coverage limitations during insurance verification

- Collect deposits for patients with temporary coverage

- Recommend ACA-compliant alternatives when appropriate

- Flag short-term insurance in billing systems for enhanced monitoring

Catastrophic Health Insurance: High-Deductible Implications

Financial Impact on Medical Practices

- Catastrophic plans require patients pay 100% of costs until meeting deductible

- Average catastrophic plan deductible in Texas: $9,450 (2025)

- Collection challenges: patients often unable to pay full charges

- Payment plan requests increase by 156% with catastrophic coverage

DFW-Specific Resources: Building Your Patient Support Network

Healthcare Infrastructure Advantages in Wylie and Greater Dallas

Local Enrollment Assistance Programs:

- Community Health Centers providing marketplace enrollment help

- Certified navigators available at no cost to patients

- Texas Department of Insurance consumer helpline: 1-800-252-3439

- Healthcare.gov special enrollment period verification

Provider Partnership Opportunities:

- Develop relationships with local insurance brokers for patient referrals

- Partner with community organizations offering benefits counseling

- Create resource handouts with DFW-specific enrollment contacts

- Host insurance education workshops at your practice

Gig Economy Health Insurance Considerations:

- Growing number of independent contractors in DFW area need individual coverage

- Freelance and contract workers represent 36% of Texas workforce

- These patients often experience multiple coverage transitions annually

Health Insurance Gap Coverage: Preventing Revenue Loss and Patient Abandonment

Emergency Health Coverage Strategies

For Healthcare Managers:

- Implement 30/60/90-day insurance expiration alerts

- Proactive outreach reduces patient attrition by 42%

- Schedule follow-up appointments within coverage periods

- Provide insurance transition checklists at check-out

Revenue Cycle Protection:

- Front-end verification catches 78% of coverage issues before service delivery

- Real-time eligibility checks reduce claim denials by 31%

- Patient liability estimates improve collection rates by 24%

- Automated insurance expiration notifications reduce write-offs

Health Savings Account Options: Continuity Tool

HSA Benefits for Patients and Providers:

- HSA funds remain accessible even after job loss or divorce

- Patients can use HSA for outstanding medical bills and deductibles

- HSA-eligible high-deductible plans reduce monthly premiums

- Average HSA balance: $4,318 (provides payment cushion during transitions)

Practice Considerations:

- Accept HSA cards for copays, deductibles, and services

- Educate patients on using HSA funds for transitional coverage

- Provide detailed itemized statements for HSA reimbursement

Action Plan: Implementing an Insurance Transition Support Program

For Medical Practices and Clinics

System Setup (Weeks 1-2) – Phase 1:

- Configure practice management system alerts for insurance expiration dates

- Create standardized scripts for front desk staff

- Develop patient resource handouts with local enrollment contacts

- Establish relationships with insurance brokers and navigators

Staff Training (Weeks 3-4) – Phase 2:

- Train front office on special enrollment periods and qualifying events

- Educate billing staff on COBRA continuation and marketplace plan verification

- Create reference guides for common insurance transition scenarios

- Role-play patient conversations about coverage changes

Patient Communication (Ongoing) – Phase 3:

- Send 90-day advance notices before COBRA expiration

- Provide marketplace enrollment deadlines at every appointment

- Offer extended payment plans for patients in transition

- Schedule appointments strategically within coverage periods

Measuring Success

Key Performance Indicators:

- Patient retention rate during insurance transitions (target: >85%)

- Average days to coverage resolution (target: <30 days)

- Insurance-related claim denial rate (target: <5%)

- Accounts receivable aging for transitioning patients (target: <60 days)

- Patient satisfaction scores regarding insurance support

Take Action Now: Stop Revenue Loss from Insurance Gaps in Your Practice

Don’t let patient insurance disruptions devastate your practice revenue and patient relationships.

This Week:

- Schedule staff training on special enrollment periods and COBRA coverage

- Update patient intake forms to capture qualifying life events

- Establish relationships with 2-3 local insurance enrollment specialists

- Review your practice’s network status with major DFW marketplace carriers

This Month:

- Implement automated insurance expiration alerts in your practice management system

- Create patient resource materials specific to Texas marketplace options

- Develop standard operating procedures for insurance transition support

- Analyze revenue impact from insurance gaps over the past 12 months

External Resources:

- Healthcare.gov Special Enrollment Periods – Official marketplace information

About Supporting Patients Through Life Transitions

Healthcare providers in Wylie and the DFW area face unique challenges when patients experience major life changes. By proactively addressing insurance transitions, medical practices can maintain patient relationships, protect revenue, and provide the continuity of care that leads to better health outcomes.

Our commitment to healthcare providers includes ongoing education, practical resources, and partnership opportunities that strengthen the connection between patients and their medical homes—regardless of insurance status changes.

Integrate Point helps Texas, US healthcare providers prevent claim denials, reduce bad debt, and retain patients during insurance transitions through real-time eligibility verification and revenue cycle support.