Even when patients have primary Healthcare insurance, clinics still face unpaid balances, surprise bills, and lengthy collections that eat into revenue. Supplemental insurance can reduce patient out-of-pocket costs and protect your practice’s cashflow, but it isn’t the right solution for every patient.

This guide explains what supplemental plans cover, how they affect patient responsibility (deductibles, copays, coinsurance, out-of-pocket costs), and the practical steps clinics and practice managers can use to verify coverage, reduce write-offs, and improve patient satisfaction.

What is Supplemental Health Insurance?

Supplemental insurance is additional coverage purchased to cover gaps left by primary Healthcare insurance. For patients it reduces direct costs (deductibles, copays, coinsurance); for clinics it reduces the risk of unpaid balances and improves collections. Common out-of-pocket items supplemental plans help with include:

- Deductibles

- Copays and Coinsurance

- Dental & vision services not in primary plans

- Certain hospital, accident, and critical-illness costs

Types of Supplemental Insurance

There are various supplemental insurances available for people with other health plans that can provide extra coverage for various healthcare needs. Here are some common types of supplemental insurances:

Dental and Vision Insurance

It offers coverage for dental and vision care that you can purchase as a separate supplemental insurance. Many health plans do not cover dental and vision care, while sometimes it is also offered as a part of primary health insurance plan.

Hospital Indemnity Insurance

Also known as Hospitalization insurance, offers a fixed amount of cash benefit to cover the medical expenses if you are hospitalized due to serious illness or injury. These plans can help share the out-of-pocket costs such as deductibles, copayments, and other costs relating to a hospital stay.

Critical Illness Insurance

provides coverage if you’re diagnosed with a specific critical illness, such as cancer, heart attack, paralysis, renal failure, or stroke but it is not covered by your main health plan. Critical illness policies offer a lump sum which can be used for anything, like insurance out-of-pocket costs, rent and mortgage payments, childcare and groceries while you recover.

Accident Insurance

Offers to cover medical expenses and out-of-pocket costs that are associated with an accident, such as emergency treatment, hospital stays, and follow-up care. It helps cover costs related to accidental injuries such as burns, broken bones, disability, going blind, concussions and paralysis.

Long-Term Care Insurance

Covers the costs of long-term care services, such as nursing home care, adult daycare, assisted living facilities, or home health care.

Disability Insurance

Provides you a portion of your regular income if you become disabled and can’t work. You can get coverage for both short and long periods of disability, you will receive payments until your benefits period ends or when you’re fit to work again.

Why clinics should care: Patients with appropriate supplemental coverage are more likely to pay balances and keep appointments, reducing administrative collection time and improving clinic cashflow.

Medigap plans (Medicare Supplemental Insurance Plans)

Medigap (Medicare Supplement Health Insurance), also known as Medigap plans and are designed to fill the “gaps” in Original Medicare (part A and part B) coverage. It protects you from financial burdens that come along as unexpected costs.

Medigap Plans Benefits for Patients and Clinics

Key Benefits of Medigap plans:

- Guaranteed Renewability Every Year: Your coverage continues year after year if you pay your premium. Only in rare cases like application inaccuracies, can it be cancelled.

- Clear and Simple Plan Options: Since Medigap plans are federally standardized, comparing and choosing the right plan is easier.

- Access to a Nationwide Network: You can visit any doctor or specialist in the U.S. who accepts Medicare, no referrals or network restrictions. The providers who accept Medicare must accept all Medigap plans, regardless of the insurer.

- Greater Flexibility in Your Care

Unlike some Medicare Advantage plans, Medigap allows you to choose any treatment option or a primary care physician you prefer.

Benefits for Patients: predictable coverage, less cost exposure, nationwide provider access.

Benefits for Clinics: fewer patient balance disputes, lower risk of unpaid claims, and simpler billing when a patient has Medigap.

Action for Clinics: ensure your intake team asks Medicare patients whether they have a Medigap plan, capture plan name & policy number, and verify benefits before non-emergency procedures.

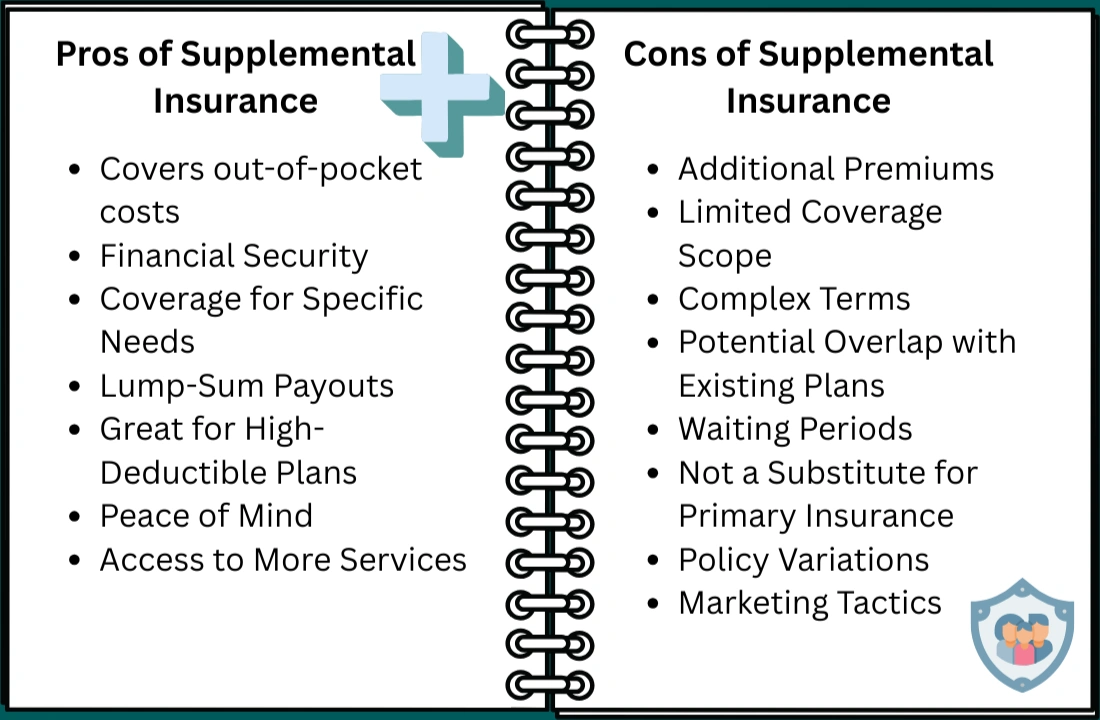

Pros and Cons of Supplemental Insurance

To help you determine if it’s the right fit for your healthcare needs:

Pros (Patient view):

- Reduces large out-of-pocket costs for hospital stays and critical events.

- Pays lump sums for covered critical illnesses (can be used for medical or living expenses).

- Covers services not in primary plans (dental, vision, some rehab).

- Provides peace of mind for high-risk patients.

Pros (Clinic / Practice view):

- Fewer unpaid patient balances and lower collections workload.

- Faster eligibility verification and clearer billing outcomes.

- Improved patient retention and satisfaction because surprise bills drop.

- Potentially fewer denied claims that turn into write-offs.

Cons (Patient view):

- Additional monthly or annual premiums.

- Policy complexity, some services still not covered.

- Overlap with employer benefits can make some policies redundant.

Cons (Clinic / Practice view):

- Patients may be confused about coverage and expect clinics to “fix” uncovered balances.

- Administrative time required to verify supplemental benefits and educate patients.

- Some patients decline supplemental plans due to cost, keeping the collection risk.

How to Decide Checklist

For Patients:

- Review primary Healthcare insurance: identify deductibles, copays, coinsurance, and exclusions.

- List regular prescriptions and treatments; check plan formularies and coverage tiers.

- Compare supplemental premiums vs potential annual out-of-pocket savings.

- Consider life stage & financial tolerance: retirees and chronic conditions often benefit more.

- Ask your clinic’s financial counselor about common local out-of-pocket items.

For Clinics / Practice managers:

- Add a supplemental-coverage question to intake forms (plan name & policy number).

- Train front-desk to verify Medigap / supplemental benefits during scheduling.

- Offer pre-visit financial counseling for high-cost procedures.

- Integrate supplemental checks into your eligibility verification workflow to reduce denials.

- Track write-offs tied to lack of supplemental coverage and report monthly to identify trends.

FAQ

Do I need supplemental insurance if I already have Medicare?

If you have Original Medicare and want lower copays/coinsurance, Medigap plans often help — but evaluate premiums vs expected annual out-of-pocket costs.

Will supplemental insurance pay my entire hospital bill?

Some supplemental plans (e.g., hospital indemnity) pay fixed benefits that help with hospital costs but rarely cover 100% of every bill — check policy details.

How can clinics verify supplemental coverage before appointments?

Capture plan details at intake and use insurer portals or phone verification. Integrate Point can automate these verifications for practices.

Does having supplemental insurance guarantee no surprise bills?

No, but it significantly reduces the likelihood and amount of surprise bills when used correctly.

Conclusion:

Supplemental insurance (including Medigap plans) reduces patient out-of-pocket exposure and lowers the risk of unpaid patient balances — a direct win for clinic revenue and operations. While supplemental plans add premium costs for patients, the net effect for clinics is clearer collections, fewer surprise bills, and smoother billing workflows.

Integrate Point helps clinics in Texas verify supplemental coverage, perform pre-visit eligibility checks, and implement revenue-cycle improvements that reduce write-offs and improve cashflow. To set up automated verifications or financial counseling workflows for your practice, visit Integrate Point or contact our team.

I regard something genuinely special in this site.

We are happy to hear that😊

I am usually looking for brand spanking new information on this

kind of crucial subject matter, and was specifically stoked the moment

I actually discover sites that are well-written and well-researched.

I want to thank you for providing this exceptional info,

and i also glimpse onward to read more from your weblog in the future.